COMMERCIAL IN CONFIDENCE

FEASIBILITY STUDY

Opportunities for Export Log Movement on Rail in

Taranaki -Whanganui

June 2020

1 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

link to page 3 link to page 5 link to page 6 link to page 7 link to page 12 link to page 16 link to page 21 link to page 21 link to page 22 link to page 25 link to page 28 link to page 29 link to page 29 link to page 29 link to page 31

COMMERCIAL IN CONFIDENCE

Opportunities for Export Log Movement on Rail in Taranaki-

Whanganui

CONTENTS

1.

Background .................................................................................................. 3

2.

Logs on rail ................................................................................................... 5

3.

Taranaki- Whanganui forestry - currently ..................................................... 6

4.

Future sources of logs in Taranaki-Whanganui ............................................ 7

5.

Resources needed to transport logs by rail ................................................ 12

6.

Potential rail log hub sites .......................................................................... 16

7.

Estimates ................................................................................................... 21

8.

Haulage costs ............................................................................................ 21

9.

Externalities: costs borne by the communities ........................................... 22

10.

Stakeholders .............................................................................................. 25

11.

Risks .......................................................................................................... 28

12.

Summary .................................................................................................... 29

13.

Conclusions ................................................................................................ 29

14.

Recommendations and next steps ............................................................. 29

Appendix 1: Stakeholder Engagement ................................................................. 31

2 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

1. Background

The purpose of this report is to investigate the feasibility of establishing a log handling facilities and

rail services for logs in Taranaki. Its conclusion is that there is scope for such rail services in

Taranaki. It recommends that KiwiRail confirms a site at Waverley, and that it works with forest

owners to confirm its viability, and develops detailed operational plans. KiwiRail should apply to the

Provincial Growth Fund for funding to develop the hub.1

Haulage of logs is a significant part of the total freight task in New Zealand. The National Freight

Demand Study 2017/182 shows that in that year they made up 13% of the total tonnes hauled, and

14% of the total net tonne kilometres.3 Rail’s share of that log market was 10% (in ntkm). Then rail

carried 3.2m tonnes of logs, principally in the Bay of Plenty, and generated 423m ntkm.

The volume of logs cut has risen significantly since the second NFDS in 2012, and so has log

transport. As a result of past planting patterns, the so called “wall of wood” is now with us. The NFDS

shows a plateau of log availability until 2032, followed by a 10 year decline before newer plantings

become available (see Figure 1).

Figure 1: 2015 Wood availability forecast by region.

40.0

Southland

35.0

Otago

s) 30.0

Canterbury

e

n

n

West Coast

to 25.0

(m

TNM

st

e 20.0

Wellington

v

ar

h

Manawatu

g 15.0

o

Taranaki

tal l 10.0

To

Hawke’s Bay

Gisborne

5.0

Bay of Plenty

0.0

Waikato

2017

2022

2032

2042

2052

Source: Ministry of Transport, National Freight Demand Study 2017-18 (“NFDS 3”), Fig 7.5, p 84

Note that there is no growth in the years after 2042 in the Manawatu - Whanganui and Taranaki

regions. The data in Figure 1 for these regions is shown more clearly in Figure 2.

1 See further detail in Section 12.

2 Ministry of Transport,

National Freight Demand Study 2017-18, (NFDS3)

3 Based on an unpublished estimate of 40.08 bn ntkm of logs

3 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 2: Wood availability in western NI

Taranaki, Whanganui-Manawatu wood availability

3.0

2.5

2.0

m,s 1.5

e

Manawatu-Whanganui

n

n

Taranaki

to 1.0

0.5

0.0

2017

2022

2032

2042

2052

Source: R Paling, inputs to NFDS3, Fig 7.5

The Manawatu-Whanganui region is large in area, and its average figures may not represent the

specific pattern in the Whanganui District, part of which is the source for the logs that would use a

south Taranaki log hub. The Whanganui patterns will be discussed below.

The wood availability figures are however based on plantings and growth; harvest levels can vary

for several years around the availability date, to match demand and the availability of harvesting

resources. This is illustrated in Figure 3.

Figure 3: Alternative log harvesting scenarios4

60000

Scenario 1

Scenario 3

50000

Actual

40000

NFDS forecast

3

m 30000

000

20000

10000

0

14

16

18

20

22

24

26

28

30

32

34

36

38

40

42

44

46

48

50

52

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

20

Source: NFDS3, Fig 7.4, p 84.

Most of the increased log movement during the period will be for export, with exports falling off even

more sharply in the 2030s, as preference is given to supplying local processing plants. The current

4 ”Scenario 1” and “Scenario 3” are scenarios from the MPI Wood Availability Forecasts. There are 4 scenarios in this report, and

Scenario 1 was chosen in the NFDS as an unconstrained scenario, when the smaller forest owners are assumed to harvest their

forests when these reach an optimum age, and scenario 3 as a more stable one constrained by harvesting and transport

resources. See NFDS3, above n 2, pp 81-82

4 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

growth in log exports is the difference between a rapidly increasing harvest and a relatively constant

local demand.5 While the balance between exports and local demand is also influenced by price, it

is expected that at least major plants will still need supply and their willingness to pay will reflect

that.6

The current wood availability is driving new value-add processing such as is proposed at Marton,

which is likely to have a longer planning horizon that 2032 and so will expect to be supplied in the

lower-volume years.

KiwiRail has opened new locations for log haulage in recent years, especially in the southern North

Island7 and could open more with the increase in log availability. These have shown substantial

growth, and one has had to be extended. One of the new areas currently and with significant growth

potential is Taranaki-Whanganui.

2. Logs on rail

Rail has had extensive experience in hauling logs in many parts of the country throughout its history,

with significant recent growth. In the year ending 30 June 2019 it hauled 3.6 million tonnes of logs,

principally in the Bay of Plenty, but also to the ports of Napier, Wellington, and Lyttelton. Most logs

hauled by rail are for export.

Table 1: Logs by rail in 2018-19

Route

Tonnes (m)

Waikato and Bay of Plenty to Tauranga

2.759

Southern North Island to Napier and

0.740

Wellington

West Coast to Lyttelton

0.064

Other

0.043

Total

3.606

Source: KiwiRail

For most flows outside the Bay of Plenty KiwiRail has been using former 50ft container flat wagons

converted to log wagons by the addition of cradles.

They will be replaced with new container wagons fitted with

“cassettes”8 and cradles, the FIH class. These can carry up to 52.5 tonnes of logs, but they are likely

to be limited to one truck and trailer load, 32t,9 to enable log traceability, at least initially. 32t tonnes

is the load per wagon assumed in this study. These wagons and cassettes are underway and are

expected to be delivered during 2020.

5 NFDS3, above n 2, Figure 4.5, p 15

6 Local supply will also be encouraged under the Forest (Regulation of Log Traders and Forestry Advisers) Amendment Bill,

currently before the House.

7 Waingawa (Masterton) 2012, East Town (Whanganui) 2015, Feilding 2020 and Wairoa 2020.

8 Bases to adapt cradles and cradle spacing to the standard container twistlocks on the wagon, and to provide walkable decking

for scaling etc.

9 Typical HPMV log load

5 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

3. Taranaki- Whanganui forestry - currently

Within the southern North Island forest group are substantial flows of logs already moving from

Whanganui to Napier and Wellington, totalling 112,400 tonnes in 2018-19.10 These logs are loaded

at KiwiRail’s forestry hub at East Town (Whanganui)11, and move on daily trains to the respective

ports, in equal volumes to each of them. Since September 2019 a new route from East Town to New

Plymouth has been established, with relatively low volumes.12

The growth in forestry in the Whanganui District and Taranaki Region in the next three years and

beyond offers the potential to substantially grow this business.

Movement of logs through Port Taranaki has grown strongly in recent years.

Table 2: Export Logs via Port Taranaki

Calendar Year

Export logs (tonnes)

2013

295,998

2014

232,896

2015

280,735

2016

406,439

2017

593,522

2018

785,183

2019

881,879

Source: Statistics NZ International trade data, commodity 4403. 2019 is provisional.

The proportion sourced from the Whanganui area is currently about a third. This is likely to grow as

Port Taranaki is closer to Whanganui than is Napier or Wellington.13 Port Taranaki has re-organised

its Blyde Wharf to cope with the log traffic,14 and has adequate room and facilities to handle the

growth in logs. However, when there are two ships on the berth, rail operations impede loading and

have to cease. An expansion of the adjacent rail grid, to separate rail and shipping, is part of this

proposal.

Only a small fraction of these logs have so far been carried to Port Taranaki by rail; up to September

2019 all came by truck, and most continue to do so. There is thus an opportunity for rail to increase

its share of the trade. The forest distribution in the region (see map, Figure 4 below) indicates that

virtually all of these logs would have been hauled through New Plymouth to get to the port, and

through other communities as well.

Local communities are concerned with the disruption that significant logging truck movements are

likely to cause, to amenity values like safety and environment, including greenhouse gases, to

congestion, and to the impact on local road maintenance.15 These “externalities” are not borne by

the log owner or transporter, but by the community as a whole. Haulage by rail will avoid having log

trucks pass through some urban areas, particularly central New Plymouth. The externalities are

quantified later in this report.

10 The remainder of the southern NI logs in Table 1 move from Palmerston North and Waingawa.

11 See Figure 12.

12 6 wagons/day pre Covid-19

13 Port Taranaki is 171km from East Town by rail, Napier 237km, and Wellington 220km.

14 “New daily log service to Port Taranaki”,

Taranaki Daily News 7 October 2019

15

Taranaki Daily News, above n 14.

6 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

KiwiRail’s experience in hauling logs is that it is difficult to be competitive with road transport over

distances below about 75km by rail. For both road and rail haulage, the logs are taken out of the

forest by truck, up to 50 km from the rail transfer point. Rail is competing against the marginal cost

for a truck to continue its journey to the port. In addition there are transfer costs for rail, but not road,

which are independent of distance, and thus form a greater proportion of the cost of short distance

journeys.16

That means that the logs from New Plymouth District are unlikely to be hauled by rail, but some in

the Stratford and South Taranaki Districts could be. A distance of 75km from Port Taranaki includes

the Marton-New Plymouth line as far south as Normanby; and the Stratford-Okahukura line

(currently mothballed) as far inland as Huiroa.17 Any movement of logs sourced north or west of the

75km line on Figure 4, and as well forests near that line, is not likely to be competitive by rail. All of

the Whanganui District is well beyond 75km from a port. Even at distances beyond 75km, the margin

over road is slender, especially if the cost of establishing a terminal has to be included.

4. Future sources of logs in Taranaki-Whanganui

The likely sources of logs that are open to rail haul are in 3 groups: the Te Wera forest inland from

Stratford; the southern South Taranaki District and the western part of Whanganui District; and the

eastern part of Whanganui District.18 A further 240,000t pa from the Taumarunui area could move

to Port Taranaki by rail if the Stratford-Okahukura line was reopened fully, but this traffic is outside

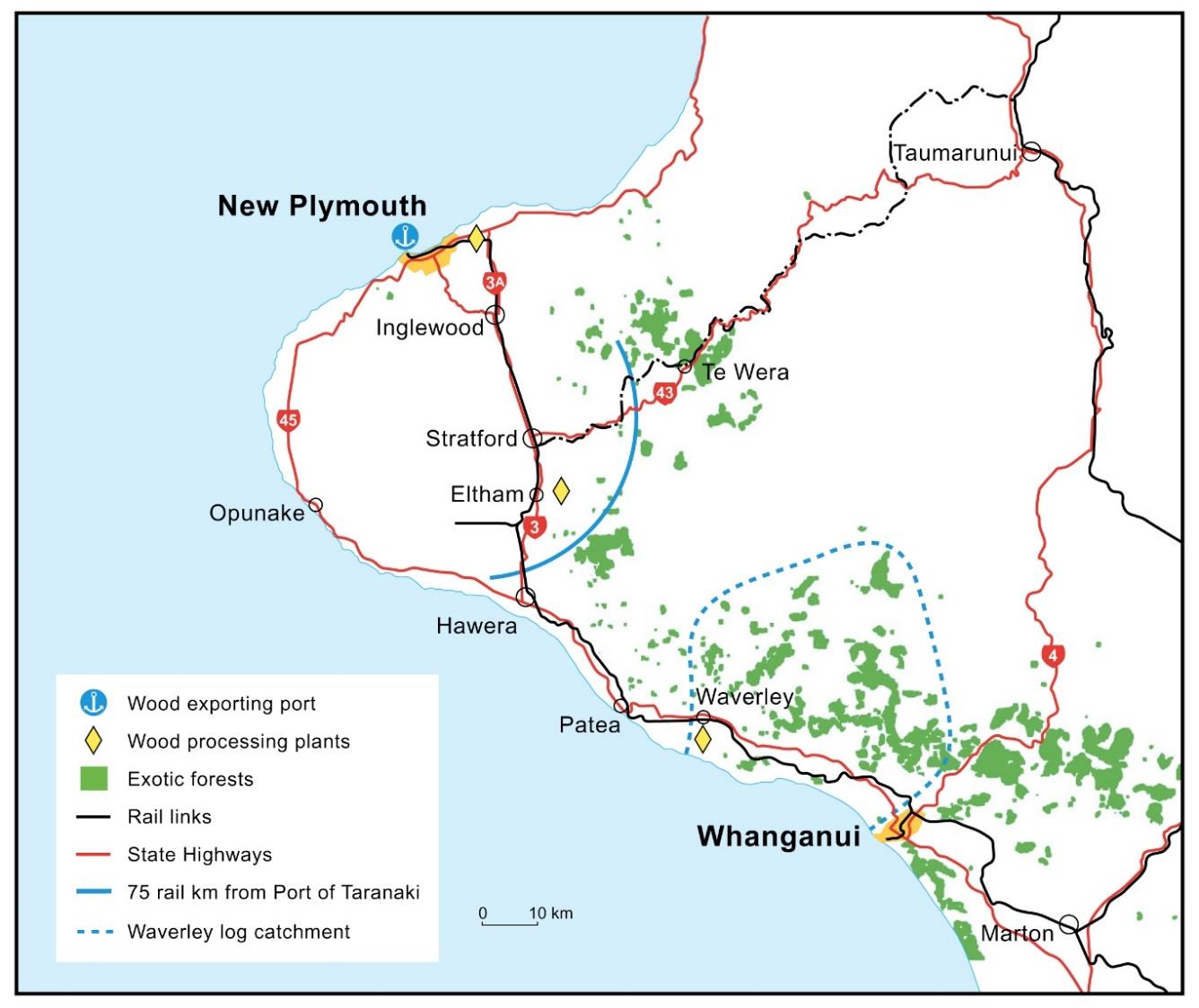

the scope of this report. Figure 4 shows the location of exotic forests in Taranaki-Whanganui, rail

lines, and 75km from the port by rail. It also shows the estimated catchment area for a Waverley log

loading point.

16 See also Figure 16. The shortest rail haul for logs in New Zealand at present is Kawerau-Mt Maunganui, 84km. This is however

an easily graded route which allows highly efficient trains of 2400t gross each (potentially about 1700t of logs, or 53 truck and

trailer loads.)

17 75km by State Highway extends slightly further, to Hawera and Strathmore respectively

18 The division of Whanganui into two groups is to identify those logs that would be more effectively served by a western

Whanganui log yard. The dividing line between Whanganui west and east is essentially the Whanganui River, though Moore’s

Kauarapoao Group on the true right (west) bank of the river is included in eastern Whanganui as the roading patterns make East

Town the logical loading place. See Moore and Associates, “Review of wood availability and related roading implications on

Whanganui District Roads 2018-2047” (2017)

7 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 4: Taranaki and Whanganui exotic forests

Source: Based on MPI: Southern North Island Wood Supply Region. Excludes forests outside Taranaki/Whanganui.

The Te Wera forest is on the cusp of the 75km competitive distance. It is 88km by rail to the port

from the former rail siding at Te Wera, but only 80km by state highway. Further forest blocks near

Strathmore are likely to be under 75km from the port.

The owners of the Te Wera forest announced in 2018 their intention to cut at least 100,000t a year

for 7 years.19 Approximately 20% of this is earmarked for Taranaki Pine’s Bell Block mill, leaving

some 80,000t pa for export. While it could be physically possible to haul the Te Wera logs by rail,

the low volumes and short life make it unlikely to be uneconomic, especially since it would require

the reopening of 37km of the Startford-Okahukura line. It is not planned to reopen the whole line, so

reopening to Te Wera would be a charge to the project.

The Whanganui west/southern South Taranaki volumes are greater, and at a more competitive

distance from the port (about 120km by rail). There is a much stronger case for hauling these by rail

than for the Te Wera logs.

19 China Forestry Group, press release 16 November 2018. We have no information on further cut, but age structure information

suggests further years’ cut would be low.

8 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

The raw data for logs becoming harvestable is shown in Figure 5, in three-year groups. The available

volume is very sharply peak in the years 2024-2029. These figures are net of the allowance for local

processing.

Figure 5: Raw data for log availability west of the Whanganui River

Western Whanganui log harvest

1000000

900000

800000

700000

s

600000

e

n

500000

n

oT 400000

300000

200000

100000

0

Source: Moore20 and NFED, consultant analysis

Forestry harvesters seek to smooth such peaks to make more efficient use of resources, including

labour and equipment. In addition, prices and international demand will fluctuate.21 In table 3, the

raw data for the 12 years 2024-2035 has been smoothed to indicate the likely actual harvest.

Table 3: Available export log volumes in southern South Taranaki, and western Whanganui

Districts with smoothed peak

Year

Available volume (tonnes) Volume per year

2018-2020

109,213

36,404

2021-2023

122,304

40,768

2024-2026

539,022

179,674

2027-2029

539,022

179,674

2030-2032

539,022

179,674

2033-2035

539,022

179,674

2036-2038

186,699

62,233

2039-2041

268,213

89,404

2042-2044

322,697

107,566

2045-2047

624,273

208,091

Source: Moore and NEFD; consultant analysis

These figures have been adjusted for the expected local processing volume, assessed at 12.5%22

of the initial (2018-2020) volumes, every year. We are not aware of any significant new processing

plants in the area which could absorb 12.5% of the later years’ peak cut, except possibly a proposed

Marton plant. However, we believe this is likely to draw its supplies from forests closer to the plant.

20 See n 18

21 Moore, above n 18, p5

22 Advice from I Moore, (10-15%)

9 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

The figures also do not take account of the current intensive planting programme organised by the

Government (“one billion trees”). We have consulted with Te Uru Rākau/ NZ Forestry over the

possible impact of this programme. At present no Crown forestry commercial joint ventures for such

plantings has been signed in this area.23 In any case the logs would not be available until the very

end of the time frame in the table, and beyond. They can form no basis for investment in transport

for at least 25 years.

It is evident that there is going to be a sharp spike in demand from 2023 to 2035, even with

smoothing, after which there will be relatively low volumes until 2045. This is due to the planting

dates of the forest (in the early to mid-1990s) and is consistent with national predictions of a sharp

fall-off in available logs in total shown in Figure 1. In particular, on a national level, because of the

need to supply domestic processing plants, the volume of export logs is expected to halve.24

This in effect means that facilities developed and wagons converted to cope with export traffic will

have a relatively short economic life of about 12 years. However, the base wagons proposed are

new container wagons which can be readily repurposed over their expected 30 year life. There are

thus 3 years for planning, consenting and constructing the hub. The cutting of the peak is unlikely

to be brought forward, but there is about 40,000t pa available to carry before then if the hub is

completed early.

The existing log handling facilities at East Town in Whanganui are likely to be full with logs

generated south of the river, as discussed below.

23 Email from Sam Keenan, GM Crown Forestry, MPI, 12 May 2020

24 Ministry of Transport

National Freight Demand Study, March 2014 (NFDS2), p 255

10 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

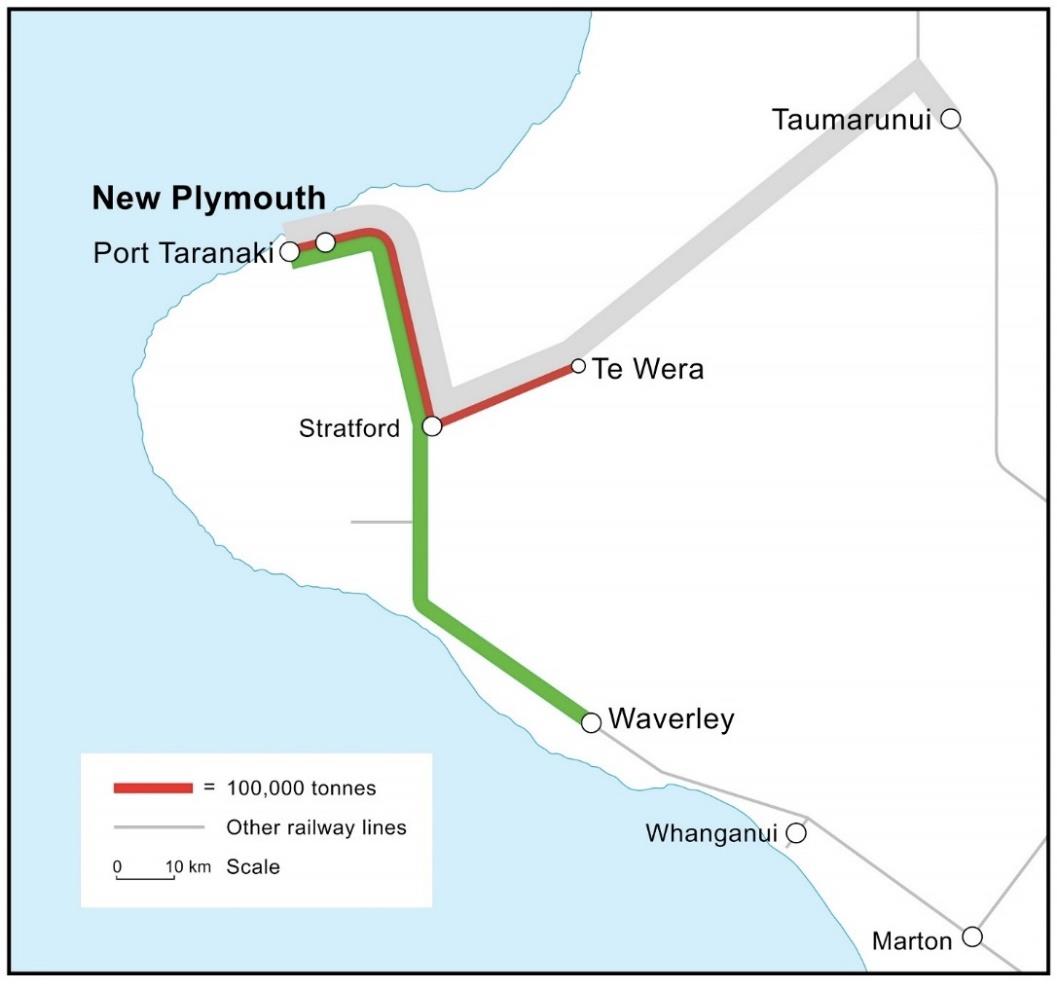

Figure 6: Potential logs flows by rail to Port Taranaki

At present the East Town facility, as expanded, can handle all the Whanganui traffic to Port

Taranaki. But volumes east of the Whanganui River, the primary purpose of the facility, are likely

also to expand rapidly, with a similar peak but with volumes 70% greater than those to the west.25

Figure 7: Raw data for logs available east of the river

Logs available east of the Whanganui River

1800000

1600000

1400000

1200000

se 1000000

n

n

800000

to

600000

400000

200000

0

25 East Whanganui volumes include the logs on the true right bank of the Whanganui, which are logically served by East Town

11 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Again the peak 12 years have been smoothed to give a better indication of the actual harvest, as

set out in Table 4

Table 4: Available export log volumes in eastern Whanganui District, with smoothed peak

Year

Available volume (tonnes)

Volume per year

2018-2020

387,866

129,289

2021-2023

127,866

42,622

2024-2026

1,058,556

352,852

2027-2029

1,058,556

352,852

2030-2032

1,058,556

352,852

2033-2035

1,058,556

352,852

2036-2038

194,489

64,830

2039-2041

403,572

134,524

2042-2044

477,962

159,321

2045-2047

627,876

209,292

Source: Moore and NEFD, consultant analysis

These figures have also been smoothed during the peak years (over 12 years), and have been

adjusted for local supply. In addition a further adjustment of 12.5% has been made to reflect

diversion of wood to supply the Karioi pulp mill, which will draw on Whanganui wood in preference

to supplies further away to the north. This adjustment is made on every year’s projected tonnage.

The strong growth especially after 2023 means that the current East Town facility is likely to be fully

loaded with traffic originating east of the river, with a potential threefold increase in throughput, and

indeed probably needing further expansion or additional sites. Thus there is unlikely to be room for

traffic originating west of the river, and a further site needs to be found to handle that traffic. Some

of this wood may also feed the proposed Marton plant, although there is a substantial volume of

local supply available to it.26

Because the East Town hub is up and running, it is not focussed on in this report.

5. Resources needed to transport logs by rail

To transport logs by rail needs a loading site, loading equipment (with staff or contractor),

locomotives (and drivers), wagons, and unloading facilities. The unloading is at the port and

assumed to be the port company’s responsibility, just as it would be for a logging truck.

At the forest end, KiwiRail has a number of former station sites that could be developed relatively

cheaply. These typically need adjustments to existing trackwork, possibly new trackwork, and a

drained metalled surface.27 Lighting would be needed for any night work. Based on Waverley, we

estimate that the cost of a hub is around

Given the profile of the log cut, the cost of these

26 Moore and Associates, “Wood availability and related roading implications on Rangitikei District roads 2018-2047”, final draft

report for Rangitikei District Council, 2017

27 Feedback from the forestry sector is that former rail yards require less drainage and surfacing work than greenfield sites

12 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

needs to be recovered 12 years. At 6% discount rate28 the annual capital cost is

As

discussed later in this report, it may be possible for local or national bodies to pay for (or contribute

to) the siding costs, reflecting the benefits they receive from rail use.

A typical log yard and siding is shown in Figure 8. This is at Waingawa in the Wairarapa. It consists

basically (right to left) of a log storage area, loading area, siding for loading rail wagons, another for

empty wagons, and the main line used by the locomotive to change ends on the train.

Figure 8: Waingawa log yard

28 Treasury transport project ra

te https://treasury.govt.nz/information-and-services/state-sector-

leadership/guidance/financial-reporting-policies-and-guidance/discount-rates

30 Source (cost and life): McCarthy Transport Ltd

31 KiwiRail’s current costs.

13 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 9: Loading logs at Palmerston North

As noted, the traffic would use FIH type wagons. These are new container flat wagons, adapted for

use in log traffic. The wagons cost

each, with the cassettes and cradles another

per wagon. While the wagons will have the normal 30 year life, there are unlikely to be any other

uses for the cassettes and cradles when no longer used for logs in this area as the same steep

decline in the cut will be experienced nationally at about the same time. For a 30 year life, the annual

capital charge at 6% would be

per wagon; with the 12 year charge for the cassettes and

cradles at

, making a total of

This is the equivalent of just over

per day per wagon. Operational constraints will mean that two

rakes of wagons34 will be required, effectively each wagon carrying a load every two days. On this

basis the capital cost is

New locomotives cost

each and have a life of 25 years. For them, an alternative use past 2032

can be assumed so their annual capital cost can be based on a 25 year life. The annual charge at

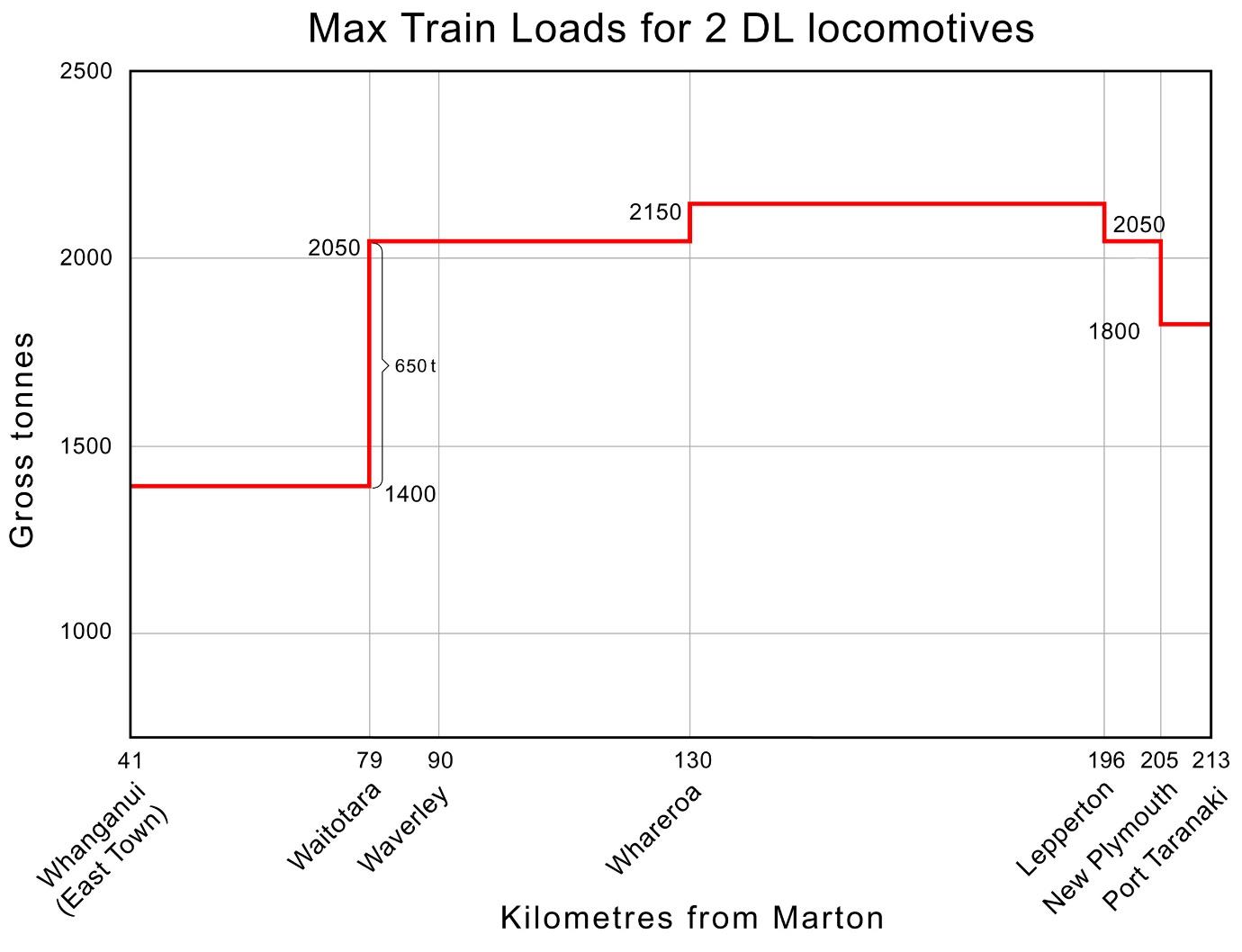

The locomotive would be one of the larger capital item in the mix, and so operational patterns have

been considered which make better use of existing locomotives. In the particular case of the line

north of Whanganui, the section from Aramoho to Waitotara has severe grades which limit the load

that can be hauled. From any location from Waitotara north to New Plymouth an additional 650t per

32 Source: Kiwirail (Alan Hill).

33

34

.

35

14 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

train36 can be carried (up to 12 loaded FIH wagons) with the same locomotive power, assuming the

normal power is two DL locomotives (see figure 8). In this cases significant efficiencies can be

achieved by more intensive use of the assets, and the capital cost for locomotives for the log traffic

is effectively nil. Their additional operating costs also close to nil (there is no increase in driver costs,

and extra fuel would be marginal). An alternative dedicated train was investigated but a competitive

price could not be reached with the forest owners.37 It would have required a new locomotive and

an additional driver.

Waverley is the nearest feasible existing yard.

Figure 10:

Offsetting the rail equipment costs will be a reduction in the number of trucks otherwise needed. A

truck and trailer can haul the same volume as an FIH wagon, so there would be a reduction of 22

truckloads a day, each way, between Waverley and the port. However, trucks will still be needed

from the forest to Waverley, some 50km. Given the likely proportion of the haul carried by rail (about

88%), and taking account of the continuing need for trucks at the forest end of the haul, the reduction

36 With a further 100t between Whareroa and Lepperton, of no use to the log traffic.

37 For discussion on competitive pricing, see section 8.

15 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

in the number of trucks needed for the traffic considered in this paper could be as much as 50%.38

Logging operators value the improved management of trucks made possible by shorter, local hauls.

By prioritising truck journeys between the forest skid site39 and a log hub, with line haul by rail,

greater volumes of logs can be transported to market while allowing truck operators to maximise

use of their vehicles. This offsets the additional costs of handling on to rail.

6. Potential rail log hub sites

Te Wera

The former Te Wera rail siding is adjacent to the Te Wera forest. It is 37 km from Stratford on the

mothballed Stratford-Okahukura line. Both the line and the siding could be redeveloped to handle

the log traffic from the adjacent forest.

Figure 11: Former Te Wera station site

Source: KiwiRail

However, the volumes are small and are expected over a short time frame (7 years), making an

investment in wagons, locomotives, and a log yard marginal. As well, the cost of carrying this traffic

would need to include the upgrading the 37km of the former Stratford-Okahukura line from Stratford,

which is estimated to cost

.

For these reasons, the traffic is likely to be uneconomic, and so the possible log yard at Te Wera

has not been considered further.

39 A ‘skid site’ or a ‘deck’ is the designated area in the forest used to further process stems or trees extracted from the forest,

store them, and then load out the logs (http://www.nzffa.org.nz/farm-forestry-model/the-essentials/roads-and-

harvesting/timber-harvesting-in-new-zealand/)

16 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

West of Whanganui River

On the basis that there is no long term room in existing East Town facilities, a new site needs to be

found for handling the western logs. All potential sites in the Whanganui city area are likely to be

needed for the traffic originating south of the river (and on the west bank of the river).

There are several former rail station sites in the area west of the river and north of the rail grades

that could be used as a log loading site. These include Waitotara itself, Waverley, and Patea.

Waitotara appears to be too small, but there is a reasonable amount of land available at both

Waverley and Patea (see figure 4). Both are only a short distance off SH3. Patea is on the banks of

the Patea River and may pose a pollution risk. It is also 14km closer to the port, making the rail

component a lower proportion of the total trip, which would be less economic for rail. This report has

used Waverley as the preferred site.

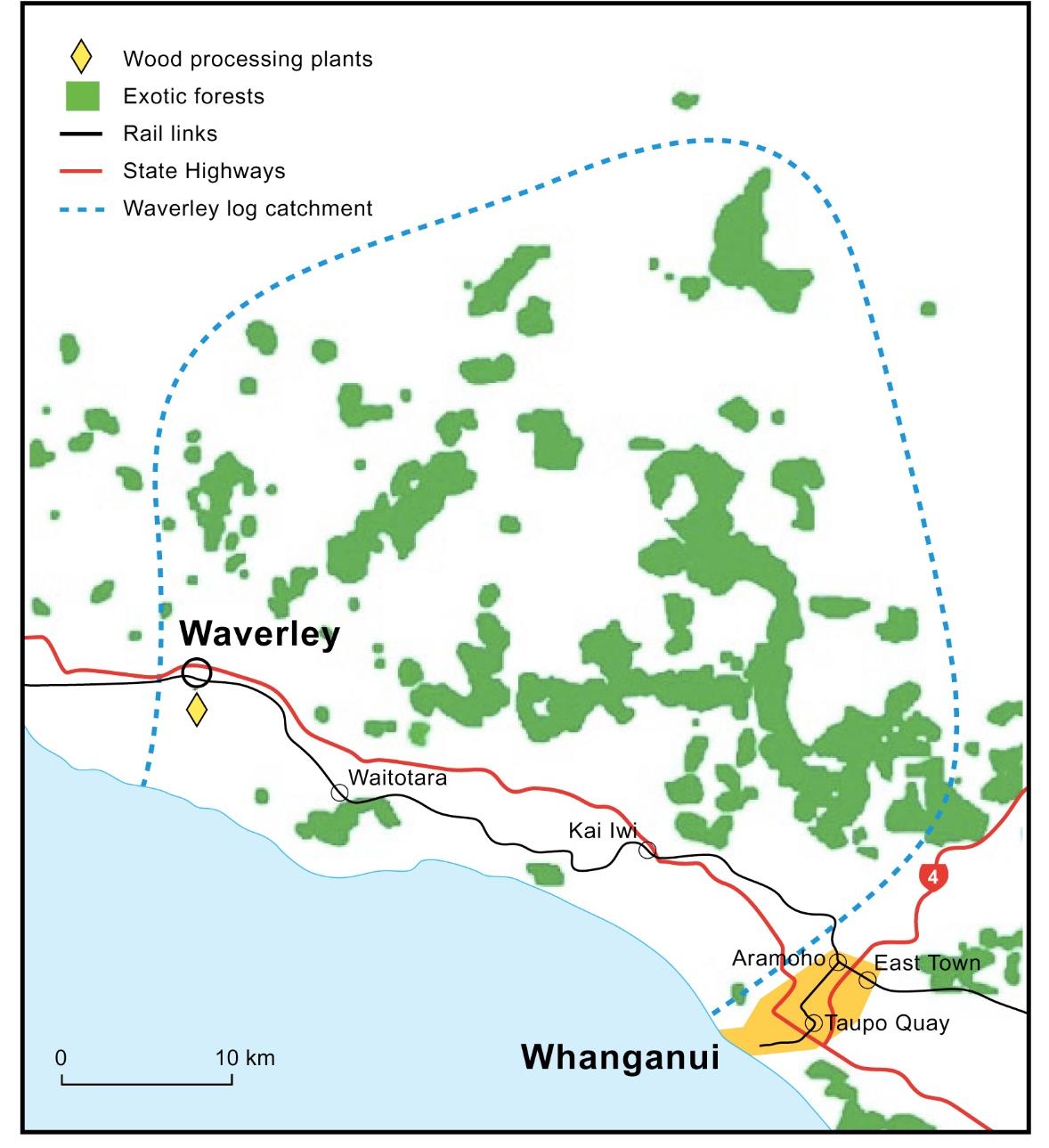

Figure 12 shows the area between Waverley and Whanganui in more detail.

Figure 12: Waverley – Whanganui locations

17 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

The volumes available from this area spread over 12 years imply a site able to handle up to 25

wagon loads per day (on a 225 day per year basis, ie 5 days/week).40 A Waverley siding would

provide for 22 wagons.41 The two daily trains would handle 11 wagons each.

Figure 13: Waverley, looking south

Figure 14: Aerial view of Waverley station

Source: KiwiRail

It is likely that two sets of 22 wagons will be required, to allow the through train to quickly swap a

loaded for a full rake. These rakes can be unloaded at the port in time to get them back for loading

in one day, and a third rake is not required. Two sets will cost

40 A typical HPMV log truck and trailer has the same 32t load as is assumed for a wagon

41 The remaining 3 wagons loads would remain for road transport. This is consistent with the practice of logging operators using

road transport directly to the port for a small number of trips per day.

42 44 wagons, 30 year life; 12 year life for cassettes and stanchions.

18 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Preliminary work on timetabling indicates that loading two 11-wagon rakes together at Waverley is

practicable. To allow loading during the day, the empty wagons will be delivered and the loaded

wagons picked up at night on the existing trains’ schedule.43 The empty wagons will need to be

staged through Waitotara to minimise the need for trackwork at Waverley.

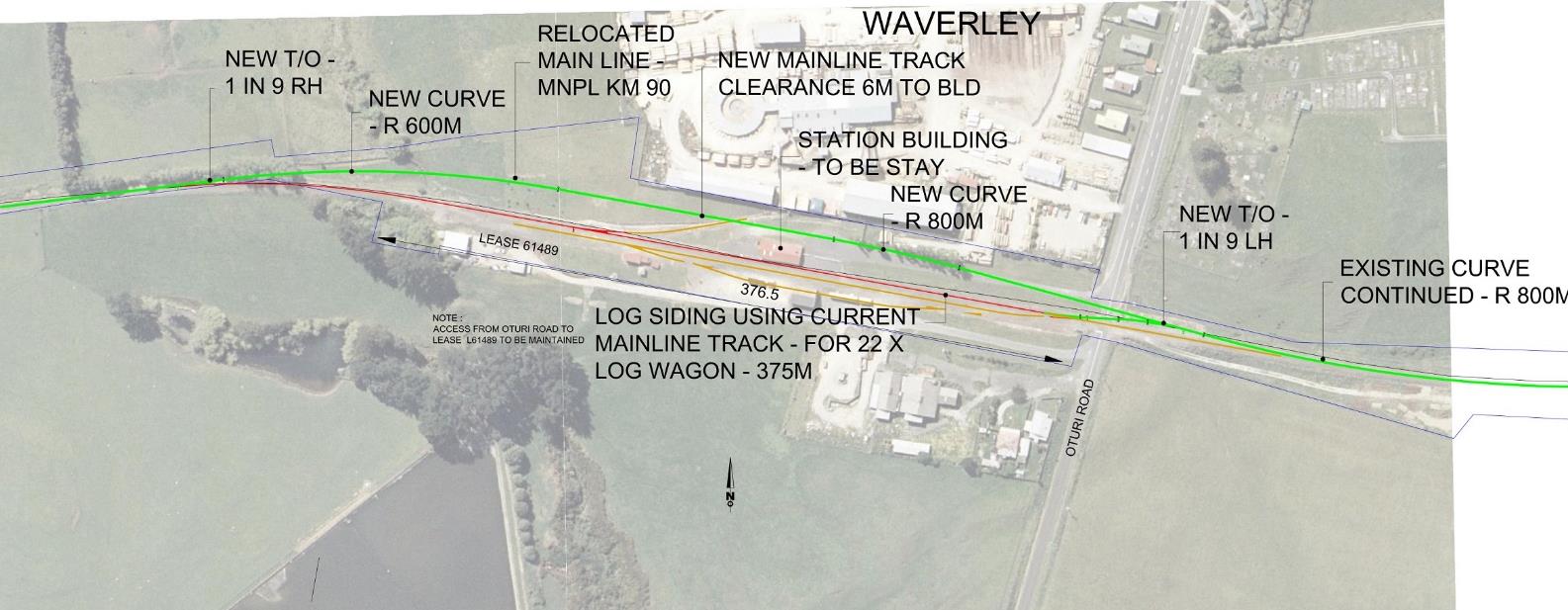

There is one primary proposal for Waverley, and a lesser alternative

The primary proposal is to re-route the main line further north, closer to the sawmill site. This lines

avoids the historic station building, but log loading would then take place adjacent to it, and arguably

put it at some risk. It would be isolated within the log yard, with no public access.44 This proposal

would cost

. It involves construction over the

sewer line to the treatment facility to the south of the station. About 300m of the sewer would need

to be replaced. As well, the main line would be more complex than the current one, with more curves.

The other proposal involves constructing a new main line 5.2m to the north of the existing main line

(to give adequate clearances for loading). The log yard would still be to the south, on the existing

yard. This proposal would mean the existing station building would need to be relocated 5.2m north,

adjacent to the new main line. Without the cost of shifting the station building this proposal is cheaper

than the other, but at an estimated

for shifting the station, the total cost is dearer at

The station building is a historic structure, built in 1881. It is one of the only two stations remaining

that were built to the standard “class 4” plan47, albeit extended and modified. The system of standard

plans dates from the Vogel era.48 The station is registered with Heritage New Zealand as a Category

1 historic place, and is listed in the District Plan as a category 1 Historic Heritage site.49

Figure 15 shows the primary proposal.

43 Their schedule is set by the needs of existing major Taranaki customers.

44 It technically has no public access now but there is a road leading to it from Oturi Rd giving de facto access.

45

46

.

47 The other is at Inglewood. Waverley is in better condition, but Inglewood is the oldest station in New Zealand still on its

original site.

48 Se

e http://www.railheritage.org.nz/Register

49 South Taranaki DC, Proposed District Plan 2015, Schedule 1, site H71.

19 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 15: Alterations to Waverley for a log yard.

Source: KiwiRail

The area available for log marshalling is limited, and may be constrained at the peak of the wood

flow.50 Existing log yards can be used as an indicator of the land required. At Waingawa a site of

about 1.5ha has a throughput of some 325,000t a year, in 10,900 wagons, 35 per day on a 7-day

basis.51 This amounts to 220,000t throughput per hectare per year. Wairoa has a yard of 1.2ha,

which has a capacity of 250,000t throughput a year, about 210,000t/ha. For the peak 12 years on

this basis the southern Taranaki log yard would need about 0.85 ha. Waverley has about 0.8 ha on

the south (goods shed) side.

These figures suggest that with appropriate realignment of the main line Waverley could cope with

the volume. If extra land is required, it would only cost about

There may also be

greenfield opportunities in the area, with land at that price not being a critical factor.

As a designated site under the RMA, an outline plan of works is required for the proposal.

Discussions with the South Taranaki District Council53 suggest that this need not be an extensive

document. They noted however that the land to the south of the station building, at least, would be

regarded as potentially contaminated, and compliance with the national standard for contaminated

land may be required (and potentially a resource consent issued).54 However, if there was no

disturbance to the soil in the area, or no spoil taken off the site, this would not be a significant hurdle.

Resource consents are also likely to be required from the Taranaki Regional Council (eg for

drainage).

South of the Whanganui River

The volumes being generated from forests in this area suggest that log handling sites will have to

cater for over three times the current volume handled, with a maximum of over 350,000t a year. The

existing site at East Town has handled about 140,000t pa in past years, and with extension could

50 Some operators work by directly loading wagons from their trucks, which means less land is required.

51 And a 45-week year, the industry standard.

52 KiwiRail Property estimate, March 2019

53 Meeting with Jessica Sorenson, Planning Manager, STDC, and other officers, 21 May 2020

54 National Environmental Standard for Assessing and Managing Contaminants in Soil to Protect Human Health (NESCS).

20 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

handle over twice that. Extending days of operation from 5 to 7 would add another 40% to the

available throughput. All that would give just under 400,000t capacity. Beyond that there is a possible

site at Taupo Quay.55 It is clear however that the East Town site will be close to capacity, and is

likely to need supplementation. It is unlikely to cope with logs from west of the river as well as those

from the east.

7. Estimates

The estimates of the operating patterns of the hubs, and their costs, are indicative only at this stage.

While they indicate that development of hubs is feasible, progressing them will require detailed

assessment of actors such as:

• Scheduling ; impacts on existing programmes

• Workforce planning

• Terminal capacity and land availability

• Landside requirements; yard size, land availability, capital investment, operation

• Asset availability and management

• Commercial factors.

8. Haulage costs

Harvested logs are a commodity product and given the time to maturity, forest owners are very price

sensitive, particularly the small-scale owners. Their price sensitivity coupled with availability of

harvesting crews affects the timing of their harvest and what they are willing to pay to transport their

logs to market. Transport decisions are largely made based on the cost of ‘stump to port’ with the

lowest cost preferred.

Traditionally the New Zealand forestry industry has relied heavily on the road transport industry to

transport harvested logs from forests to market. In many regions, road transport has been the only

option or there has been no compelling reason to choose rail given double handling costs and the

establishment costs of regional log hubs. The reason to rely on road transport is purely a commercial

decision.

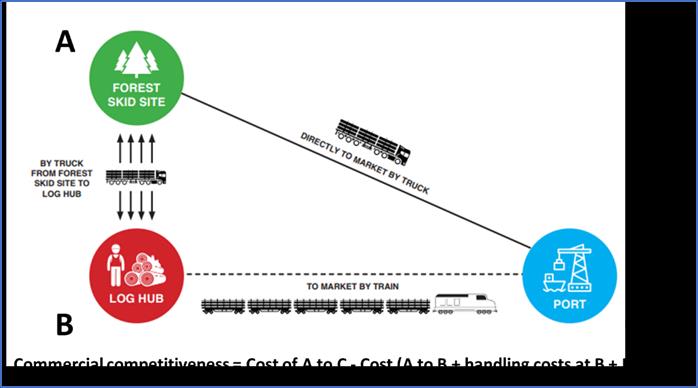

Nevertheless the establishment of strategically located log hubs enables rail to be price competitive,

and overcome the disadvantage of having to transfer from one mode to the other. This model,

illustrated in the following figure, is successfully used by KiwiRail at a number of southern North

Island sites.56

55 A further site at Aramoho has been used in the past, but the District Council refused permission to reopen it for road traffic

reasons.

56 See above, n 7.

21 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 16: Commercial issues for a rail hub

Source: KiwiRail

For the South Taranaki logs, the road haul from forest to port is 170km, and costs

From the forest to the rail yard is 50km (along the same route), and costs

. For the combined road/rail journey, the total needs to be the same or better

than the direct road cost, so the amount available for rail is the difference between these numbers,

namely

a tonne km.

From this has to be deducted the cost of handling

which leaves

for the actual rail haul.

KiwiRail’s current prices for hauling logs are

, net of handling and fuel adjustment

factor, giving revenue for this proposal of approximately

. Direct costs will be low with the

use of spare capacity on existing trains, and the traffic will cover them and make a contribution to

overheads and track (excluding the cost of developing the log yard).

9. Externalities: costs borne by the communities

As log volumes have increased, the frequency and cost of maintaining the regional road networks

has significantly increased and road safety has been negatively impacted with greater numbers of

heavy trucks on the roads. These costs will detrimentally impact the communities within those

regions (see section 10, below).

Compared with trucks, rail provides a sustainable solution will help reduce road and port congestion,

reduce the frequency and cost of road maintenance, will improve regional road safety and will reduce

carbon emissions58.

The following table with estimates of the externality costs for road and rail is adapted from Table 5-

10 in a report prepared for Environment Canterbury and SI Regional Transport Committee Chairs

by Stantec.59

57 KiwiRail, from confidential log operator source.

58 https://pro.newsroom.co.nz/articles/3728-4-are-we-ready-for-the-walls-of-wood

59 Stantec,

South Island Freight Study: Identification of the opportunity for mode shift and preparation of a mode shift

Implementation Plan 2019

22 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Table 5: Externality costs per 000 tonne kilometres

Externality costs for road and rail movements of Taranaki logs

Cost item

Road transport costs ($

Rail transport costs ($

per 1000 net tonne-km)

per 000

net tonne-km)

Urban

Rural

Urban

Rural

Greenhouse gases

3.0

3.0

0.75

0.75

Other Emissions

10.4

1.0

3

0

Other environmental

4.8

1.3

3

0

costs

Accidents

14.9

2.4

Total exc congestion

33.1

20.2

9.15

3.15

Congestion

Main

Other major

centres

urban

centres

NA

Peak

38.9

30.3

Off-peak

17.8

14.7

Rural - all areas

2.5

Source: Stantec: GHG scaled by 25% to update to 2019 levels, using EEM factors

The tonne kilometres for logs from Waverley, by road and rail, are in Table 5. The routes by rail are

slightly longer.

Table 6: Annual Tonne kilometres for log traffic from Waverley

Waverley-Port

Urban/

Taranaki

rural, %

Tonnes pa (peak years) (by rail) 158400

Kilometres (road)

119

Tonne kilometres (000) (road)

18,850

22/78

Kilometres (rail)

123

Tonne Killometres (000) (rail)

19,483

15/85

23 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Applying the factors in Tables 5 and 6 for Waverley:

Table 7: Annual Externality costs for Waverley log traffic for the 12 peak years

Externality costs for road and rail movements of Waverley logs. pa

Cost item

Road transport costs ($)

Rail transport costs ($)

Urban

Rural

Urban

Rural

Greenhouse gases

12,355

44,194

2,257

12,355

Other Emissions

42,831

14,731

9,029

0

Other

19,768

19,151

9,029

0

environmental

costs

Accidents

61,364

219,495

7,223

39,537

Total excl

136,418

297,924

27,556

51,991

congestion

Congestion

Other major

Rural

urban

centres

NA

Peak

12,479

Off-peak

54,486

Rural - all areas

36,828

Totals

203,284

334,398

27,538

51,892

Total urban and

537,682

79,430

rural

The difference between road and rail, $458,253, is the annual externality benefit of the proposal. In

principle, local and national bodies should be willing to help fund the project to gain this benefit, but

contributions from local bodies are unlikely.

In addition the Stantec report identified a contribution to the cost of roads that is not matched by

revenue from Road User Charges. This is specific to logging trucks, and relates to their practice of

loading the empty trailer on to the truck on the return from the port. Road User Charges are charged

for all vehicles, regardless of load, based on an average loading out and back, and loading the trailer

on the truck means the trailer pays the average when full, and nothing when empty. The report

calculated the revenue shortfall at 14.3 cents per vehicle km.60 There will be 22 loaded trucks/day,

225 days/year, over 119 km, and empty returns, which is just under 1.18 million vehicle km per year,

or $168,000 pa in unmet costs. These would be avoided by the use of rail

.

The net environmental and roading benefits of railing logs from Waverley are thus $626,000 a year,

for the 12 peak years. The Waverley benefits offset the annual capital costs of providing the siding

($620,000),61 and over three quarters of the total cost of Waverley and the additional capital costs

at the port ($810,000 pa in total).62.

60 Stantec, above n 59, p 26

61 Above, p 20

62 Including the port works, $0.19m pa. See below

24 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

10. Stakeholders

KiwiRail engaged with a number of stakeholders in the region. A list is in Appendix 1. KiwiRail is

grateful for their very useful inputs.

Port Taranaki

Port Taranaki has been in discussions with KiwiRail for the past 24 months about initiatives to

develop a rail option for log exports.

With greater log volumes forecasted, the Port sector generally is likely to face some constraints in

the future. The constraints will be due in part to:

- major road access corridors being through built up residential and industrial areas

- the availability and scarcity of on port land for receiving and marshalling logs

- the inability of the stevedoring and marshalling companies to man both vessel loading

operations as well as increasing road and rail log deliveries, could also impact negatively.

Ports in New Zealand aggressively compete for cargo outside their natural catchment areas to be

exported from their port. This means that at the margin, the individual growth and development

strategies around forestry and logs in particular, are commercially sensitive, and not available or

shared publicly. Port Taranaki recognise the need for investment in rail to support New Zealand’s

forestry supply chain. They supported KiwiRail’s recommendation to invest in a log hub at Aramoho

(unsuccesful) as it aligns with their strategy to extend their reach to new export customers in other

regions. They are also in support of this proposal.

Port Taranaki has upgraded its on-port infrastructure to accommodate increased volumes of logs

and in particular provide for logs arriving at the port via rail. Bringing more logs to the port through

rail would result in increased ship visits and also ease the pressure on the region's roads63.

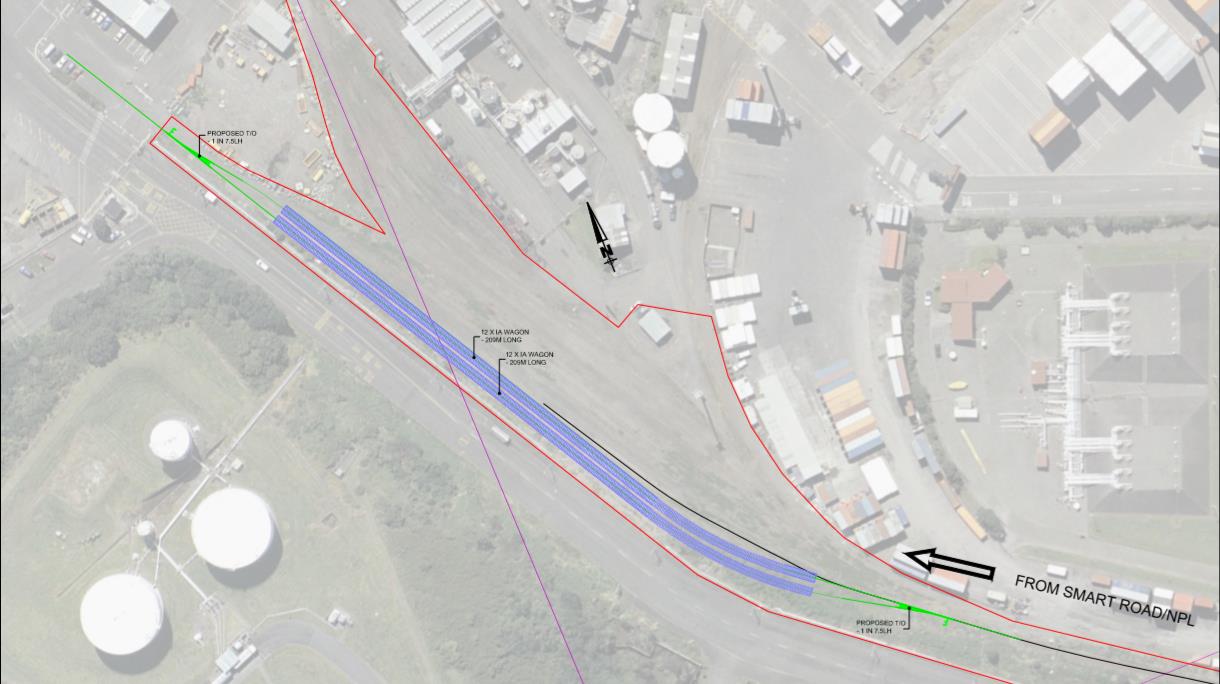

Cost of developing a rail yard at Port Taranaki

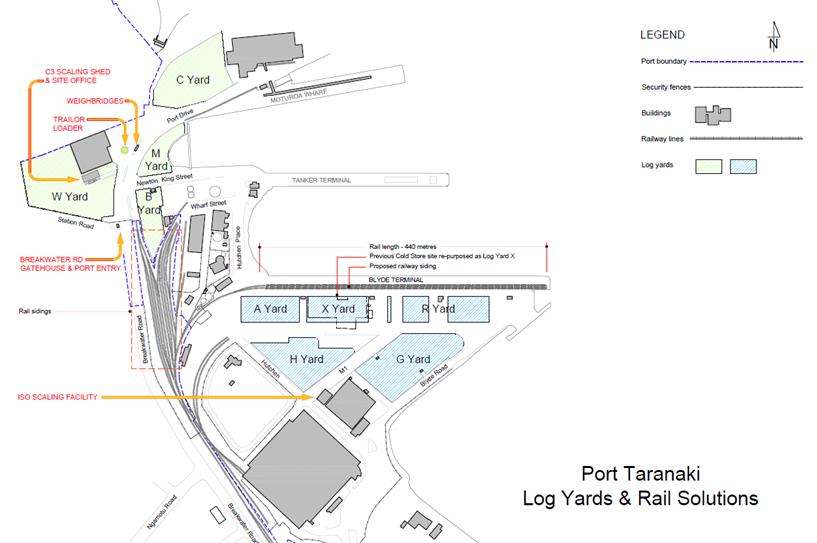

Figure 18 outlines Port Taranaki’s planned footprint for provisioning for these increased log volumes.

The costs of preparing Blyde wharf for logging traffic are being met by Port Taranaki. Kiwirail will

also have to adapt its yard at the port to handle the log traffic, at a cost of

64 as

shown in Figure 13.

63

https://www.stuff.co.nz/business/101763651/port-and-road-groups-support-taranaki-rail-network-feasibility-study

64 At 6% for 50 years. This makes the reasonable assumption that these sidings will be used for other traffics after the log peak. If

it taken just over the life of the traffic from Waverley, it is

25 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Figure 17: Alterations to rail yard at Port Taranaki

Source: KiwiRail

Figure 18: Port Taranaki Log Infrastructure Developments

Source: Port Taranaki

Taranaki Regional and local authorities

Regional and local authorities are concerned about the impact of the increased log volume by

road, in terms of public safety and deterioration of their roading assets. WSP Opus note that “By

reducing on road freight trips, a rail siding would reduce the maintenance requirements on the

26 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

surrounding road network as road condition tends to deteriorate in proportion to heavy commercial

vehicle volumes.”65

Taranaki Regional Council is aware of rising harvest volumes and is concerned about the impact

that an increased number of trucks travelling to the Port will have on regional roads and road safety.

The Council has confirmed to KiwiRail that it will strongly support any improvements to rail provision

within and to/from the Taranaki region and it notes that the current Regional Land Transport Plan

for Taranaki makes several references to the importance of maintaining and improving rail

infrastructure and services within the region.

The District councils in Taranaki and Whanganui are already seeing an increase in road

maintenance costs as a result of logging activity. Typically, in the Stratford District it usually costs

approximately $1,500 per kilometre to maintain an unsealed road. As a result of logging, that cost

can go up to about $10,000 dollars per kilometre66. However, the location of the rail network means

that it offers few alternatives to local roads; the diversion of traffic will be mainly from State Highways.

Local roads will continue to be used from forest to rail hub.

An issue of particular concern for the New Plymouth District Council is the movement of logging

trucks through urban New Plymouth en route to Port Taranaki. As volumes of logs exported via

Taranaki increases this is likely to become more problematic for the District Council and NZTA67.

The council is “highly supportive” of taking trucks off the road through the city.68 Growth in the oil

and gas and agriculture sectors is likely to place added pressure on the district’s infrastructure such

as Port Taranaki and the airport as well as the roading network that connects them with production

sites and northern and southern corridors69.

The Stratford District Council is strongly supportive of logs moving on rail.70 It is considered that

this would have a positive impact upon the impost of providing and maintaining roads with

associated environmental and safety benefits. Stratford District is part of the route from the

Whanganui forests. Similarly the South Taranaki District Council supports taking logging trucks of

the road. They too are on the route from the Whanganui forests. Heavy trucks even on the State

Highway are especially a concern in small communities like Patea and Eltham.71

The Whanganui District Council in their ‘Long Term Plan 2018-2028’ identified that the transportation

of timber associated with these harvest profiles is one of their key issues. Within this plan they have

forecast significant road maintenance and pavement renewal cost increases. The Council have

resolved to work with the forestry industry to manage their impacts on the district’s roading network

to minimise costs to be borne by ratepayers.

Industry participants

KiwiRail has consulted with several logging industry operators.

65 Traffic Impact Assessment, Rangitikei District Council Industrial Plan Change, 2019

66 https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11873074

67 Statement by District Planning Lead, NPDC

68 Meeting with Craig Stevenson (CEO) and Liam Hodgetts (Group Mgr Strategy), 2 April 2020

69 NZTA : “Keeping New Plymouth Moving and Growing” Report of December 2016.

70 Discussions with CEO, 2018

71 Meeting with Waid Crockett (CEO) and Liam Dagg,( Group Mgr, Environmental Services), 2 April 2020

27 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Forest360, a harvesting and marketing company, supports KiwiRail’s study, and is likely to be an

active participant in rail developments in Taranaki and Whanganui. It already operates a log yard at

KiwiRail’s East Town hub.

Forest Management NZ (FMNZ) support in principle any initiatives which either provide for greater

efficiency and resilience within the country’s export supply chains, or conversely contribute to

removing inefficiency.

FMNZ consider that it is counter-intuitive to be transporting logs (via any mode) from the Taranaki /

Whanganui regions for exit via other ports when a “perfectly fit for purpose port with ample capacity

is on the back door at New Plymouth.” FMNZ is encouraged that rail solutions for movement of

logs to Port Taranaki are being developed.

John Turkington Ltd (JTL) is also a forest management and marketing firm. They also use rail hubs

at East Town, Palmerston North, and Waingawa. JTL feels there are huge opportunities with rail. It

is not presently a cheaper option but offers much greater efficiencies for their road transport network.

“We would be interested in supporting an option to Taranaki provided Kiwi Rail can support it with

infrastructure, rolling stock, and people, and it does not affect our current rail business.”

11. Risks

The potential risks for the project include both construction/operational risks, and market risks.

Construction and operation

• The cost of altering Waverley exceed the contingencies. The 30% allowance should be

adequate

• Unforeseen planning issues raise the price of alterations at Waverley. The biggest planning

hurdle, the historic station, has been avoided by leaving it in situ.

• The cost of developing a log yard, especially surfacing and drainage, are more than minor,

so log operators will not pay for them. The typical experience is that former railway stations

have an adequate surface for log yard activities.

• The train operations require more sidings than allowed for. This is mitigated by the use of

Waitotara to hold empty wagons as part of the process.

• Changing exchange rates impact on wagon prices

• Changing train patterns on the Marton - New Plymouth line (which could reduce the

availability of spare capacity on trains, or could improve the wagon turnround and reduce the

number required).

Market

• The international log market, or prices, will significantly reduce

• Major new local processors take up the peak wood. This is unlikely because of the relatively

short duration of the peak (such plants need a continuous supply)

• Logging operators will not use the hub. This is unlikely, as KiwiRail has already had enquiries

about it from logging operators

28 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

12. Summary

The costs and benefits of the proposal are set out in Table 9. KiwiRail invest in new wagons, and

part of the commercial revenue goes toward paying for them. Trucks worth

are avoided.

For the PGF, an investment of $8.2m (0.81m pa) is largely offset by the community benefit of

$0.63m.72

Table 9: Summary of costs and benefits

Kiwirail

Cost

Benefit

Purchase of wagons

$8.8 m (0.71m pa)

Truck Operators

Avoided truck purchase

PGF

Alterations to Waverley

$5.2m ($0.62m pa)

Alterations at port

$3.0m ($0.19m pa)

Community benefits

$0.63m pa

13. Conclusions

The key objective of this study was to identify if opportunities exist for rail services in Taranaki (and

Whanganui) for the movement of export logs to Port Taranaki - and if so where the logical location(s)

were for the establishment of enabling rail log hubs.

There are significant forest areas due to be harvested in the area, close to rail, and over 75km from

the port.

On the basis of these forest locations and likely harvest patterns, reviews of reports, and its own

knowledge of what can be viably hauled by rail, supplemented by stakeholder engagement,

the

conclusion is that there is scope for rail services in Taranaki.

Likely sites for aggregating and transferring logs have been identified in southern South Taranaki.

The favoured site of Waverley is operationally feasible, and can be created at relatively low cost.

We have also assessed the likely benefits to communities from moving logs by rail instead of road.

These strongly support the development of a south Taranaki hub.

14. Recommendations and next steps

1. KiwiRail and industry partners to confirm Waverley as the site for a South Taranaki rail hubs,

and the rail facilities required.

2. KiwiRail to work with forestry industry parties to confirm the viability of establishing the hub, and

develop detailed plans for train operations.

3. KiwiRail to apply to the Provincial Growth Fund for funding to develop the hub in the light of its

relatively low cost, and the regional benefits that will flow from it.

72 These costs have been also calculated at discount rates of 4%pa and 8% pa as a sensitivity test. The range is about 10% either

side of the 6% rate for the short life assets like Waverley, rising to over 25% for the long life, eg at the port. At 4% the wagon

costs are

pa. The respective

; for the

alterations at Waverley $0.55m pa and $0.69m pa, and for the port $0.14m pa and $0.25m pa. The lower discount rate narrows

the gap between the PGF costs and the community benefits, and the higher one raises it.

29 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

4. KiwiRail will fund the required rolling stock and operating costs.

5. KiwiRail to engage with Waka Kotahi NZTA over the implications of developing a rail hub at

Waverley for their State Highway programme in Taranaki.

30 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

Appendix 1:

Stakeholder Engagement

Port Taranaki

CEO

Head of Commercial (2020)

CFO and Head of Commercial (2018)

Customer Relationship Manager

Cargo Services Manager

Taranaki Regional Council

Transport Services Manager

Policy Analyst

New Plymouth District Council

Craig Stevenson

CEO

Group Manager Strategy

Senior Policy Adviser

District Planning Lead

GM Innovation & Strategic Projects, Venture Taranaki

Stratford District Council

Svenne Hanne

Chief Executive

Roading Asset Manager

South Taranaki District Council

Waid Crockett

CEO

Group Manager Environmental Services

Planning Manager

Group Manager Engineering Services

Roading Manager

And other officers

Whanganui District Council

GM Infrastructure

Senior Roading Engineer

31 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui

COMMERCIAL IN CONFIDENCE

32 | © KiwiRail

Opportunities for Export Log Movement on Rail in Taranaki-Whanganui