06 August 2020

James Lochead-Macmillan

[FYI request #13301 email]

Tēnā koe James

Your Official Information Act request, reference: GOV-005765

Thank you for your email of 13 July 2020, asking for the following information under the Official

Information Act 1982 (the Act):

1.

Can you please tell me where in the ACC act, that holiday pay and redundancy payments are to

be surrendered to ACC.

2.

Also can you please explain if these payments can be used as the 20% top up to 100% pay?

3.

All documents in full, related to redundancy and holiday pay!

Accident Compensation Act 2001 – abatement of holiday pay and redundancy

The Accident Compensation Act 2001 (the AC Act), Schedule 1, clause 51(2) requires ACC to calculate a

reduction in your weekly compensation if your total earnings from weekly compensation and any other

sources take you above your normal pay level. This is referred to as abatement of weekly compensation.

Clause 49(3) of Schedule 1 of the AC Act requires ACC to take into account any payment made on the

termination of employment in respect of leave entitlements (holiday pay) when calculating abatement

of weekly compensation. Redundancy payments do not count for abatement purposes (Part 1, section

11(1)(e) of the AC Act).

Employer top-ups

Regarding your second question, we assume you are referring to an ‘employer top-up’. If an employee

is eligible for weekly compensation following an injury, their employer may make an additional payment

each week that tops-up the employee’s income during their inability to work to the level of their normal

wage, so the employee has no loss of income.

Unless an employer and an employee have contractually agreed to a top-up, any top-up is at the

employer’s discretion. However, an employee can ask an employer to pay out up to a week of holiday

pay in lieu of annual leave. Therefore, the employer and employee can agree that the employer will pay

out one day’s holiday pay per week as a weekly compensation ‘top-up’ for up to five weeks. Where an

employee is entitled to holiday pay on termination of employment, the employee and employer could

agree to structure the payment as a top-up in this way depending on how much holiday pay the

employee is owed. However, any holiday pay that an employer pays in a week that is more than 20% of

the employee’s normal weekly pay will be used to abate weekly compensation.

An employer and employee could agree to structure a redundancy payment in this way as well.

However, since redundancy payments cannot be used to abate weekly compensation anyway, this

would not provide the employee with any advantage in respect of avoiding abatement.

Policies in relation to abatement of holiday pay and redundancy

ACC’s intranet contains ACC’s policies, processes and guidance for staff working with clients. We have

attached the sections from the intranet relevant to your questions as attachments to this response (49

pages, extracted on 23 July 2020).

GOV-005765

How to get in touch

If you have any questions, you can email me

at [email address]. Nāku iti noa, nā

Sasha Wood

Manager Official Information Act Services

Government Engagement & Support

Accident Compensation Corporation

Page 2 of 2

Definition – Earnings as an Employee v9.0

Summary

Objective

Definition – Earnings as an Employee v9.0

Summary

Objective

This page provides you with the definition of 'earnings as an employee' as found in the Accident Compensation Act 2001. Use this

definition to help you determine what earnings can be included in the calculation of weekly compensation. This guidance applies to

claims where the client becomes unable to work from 1 July 2010.

1) Earnings as an employee

2) Earnings as an employee: what it does not include

3) Links to legislation

Owner

Martin Shelton

Expert

Deborah Doroshuk

Procedure

1.0 Earnings as an employee

a Sections 9-13 of the Accident Compensation Act 2001 defines ‘Earnings as an employee’, and include the following:

b Salary, wages, overtime and holiday pay, including payments for annual leave, sick leave and statutory holidays

c Allowances, including:

• accommodation allowances

• benefits gained by an employee from an employee share option or share purchase scheme

• benefit allowances, for example:

— allowance paid to an employee to work in dirty, dusty or unhygienic conditions;

— allowance paid for special duties;

— locality allowance;

— shift allowance; allowance paid to a driver who collects cash.

NOTE Allowances do not include...

Allowances do not include reimbursing allowances, i.e. money which is paid by the employer to reimburse the em-

ployee for expenses incurred by the employee on behalf of the employer, such as accommodation costs and airport

parking.

d Extra emoluments, for example:

• bonuses which are not made on a regular basis, such as an annual end-of-year bonus or a Christmas bonus;

• gratuity or any payment made in return for services, extra salary, back pay, and share of profits.

e Ex gratia payments received by an employee for past services

f Weekly compensation payments made by ACC, or an accredited employer for:

• loss of earnings

• loss of potential earning capacity

• payments made under sec ion 60 of the Accident Compensation Act 1982

NOTE Weekly compensation to spouse, child or other dependant of a person who has cover for an accidental death

These payments are not classified as earnings for the calculation of weekly compensation.

g Earnings-related compensation payments, which were payable prior to 1 July 1992

under the Official Information Act 1982

h Payments made by partnerships to ’working partners’, as defined in Section DF8 of the Income Tax Act 1994, under a written

contract of service

i All taxable payments that are expenditure on account of an employee, i.e. expenditure incurred by the employee but which is

paid for by the employer

j Payment made in lieu of, or substitution for, earnings as an employee.

NOTE Example

If a school student is in part time work, Inland Revenue may not require the employer to deduct PAYE tax, particularly

if the student earns less than $20 per week. If the employer indicates that payments have been made with no PAYE

Released

tax deduction, check with Inland Revenue to make sure these earnings are exempt, before using them for the weekly

compensation calculation.

2.0 Earnings as an employee: what it does not include

a Schedular, formerly withholding, payments which, are defined in Income Tax Act 2007 as casual payments or payments where

the relationship of the parties is not strictly one of employer-employee.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Definition – Earnings as an Employee

Uncontrolled Copy Only : Version 9.0 : Last Edited Wednesday, July 31, 2019 8:04 AM : Printed Tuesday, 4 August 2020 7:24 PM

Page 1 of 2

NOTE Example

Commissions to insurance agents or salespersons, unless subject to PAYE tax deduction, income earned by self-

employed persons, honoraria, or fees earned by entertainers, speakers, freelance journalists, models, jockeys and

trotting drivers.

b Income-tested benefits, e.g. jobseeker support, sole parent support, supported living payment, independent youth benefit, job

search allowances, training benefit

c Parental leave payments paid under Part 7A of the Parental Leave and Employment Protection Act 1987

d Any payment paid under the Compensation for Live Organ Donors Act 2016

e Veteran’s pensions, i.e. payments made to a person who served New Zealand or any other Commonwealth country as a

member of the forces, Mercantile Marine or Emergency Reserve Corps in any war or emergency in which New Zealand forces

took part

f New Zealand superannuation and living alone payments, or student allowances

g Where the client is an employee of their spouse, any amounts paid by the spouse to that person, unless the Commissioner of

Inland Revenue has consented to such amounts being earnings as an employee

h A pension paid by an employer to a former employee

i A pension paid by a business or partnership to a former partner of the business or partnership

j A pension from a superannuation scheme or pension fund that is not registered under the Superannuation Schemes Act 1989

k The following payments from insurance companies:

• weekly payments based on the client’s earnings, other than weekly compensation payable under the Accident Insurance Act

1998

• lump sum payments unrelated to earnings

• weekly payments unrelated to earnings

• retiring allowances. In the case of employees, this means any payment made, that is all of the following:

— payment to the employee in consequence of their retirement from employment with their employer

— payment that is not made on a regular basis

— a pension from a superannuation scheme or pension fund that is not registered under the Superannuation Schemes Act

1989

— redundancy payments.

3.0 Links to legislation

Accident Compensation Act 2001, section 9 Earnings as an employee: what it means

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100608.html

Accident Compensation Act 2001, section 10 Earnings as an employee: payments to spouse [or partner]

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100611.html

Accident Compensation Act 2001, section 11 Earnings as an employee: what it does not include

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100620.html

Accident Compensation Act 2001, section 12 Earnings as an employee: [Work Account] levy payable under section 168

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100632.html

Accident Compensation Act 2001, section 13 Earnings of private domestic workers

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100636.html

under the Official Information Act 1982

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Definition – Earnings as an Employee

Uncontrolled Copy Only : Version 9.0 : Last Edited Wednesday, July 31, 2019 8:04 AM : Printed Tuesday, 4 August 2020 7:24 PM

Page 2 of 2

Determine Earnings Liable for Abatement v8.0

Summary

Objective

Determine Earnings Liable for Abatement v8.0

Summary

Objective

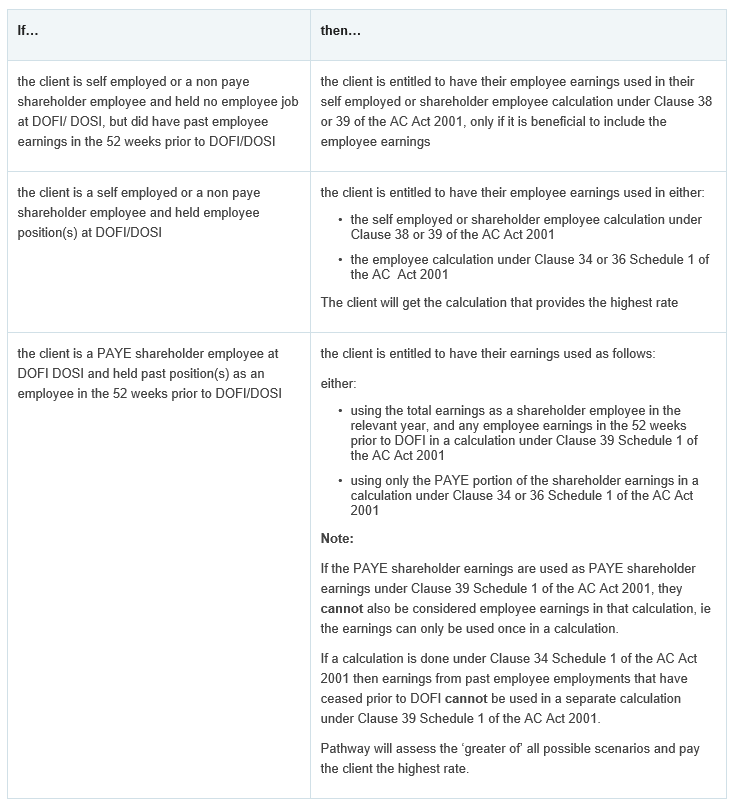

If a client receives any income during a period of incapacity, under the Accident Compensation Act 2001, Schedule 1 Clause 49, ACC

needs to consider if any part of that income is ‘earnings liable for abatement’.

If this is the case, the abatement formula is applied, which reduces base weekly compensation by a proportion of the ‘earnings liable

for abatement’.

Owner

Tui Kailahi

Expert

Nick Lamb

Procedure

1.0 Earnings liable for abatement

a The following earnings received during the client's inability to work due to their injury are earnings liable for abatement:

• wages, salary, director’s fees or self-employed earnings

• holiday pay for annual leave (if a client cannot take the leave at another time after their return to work) or statutory holidays

• taxable bonuses or one–off payments (perhaps in return for accepting a lower-paid job)

• estimated earnings of a self-employed client or shareholder employee, if actual earnings during the inability to work from that

employment cannot be determined

• any leave payments made on, or in respect of, termination of employment.

There are a number of special case scenarios when determining if earnings are liable for abatement:

• holiday pay and reinstatement of leave

• payment during the inability to work.

NOTE Special case 1: Holiday pay and reinstatement of leave

When an employer has made payment of holiday or sick pay during a period the client is unable to work, they should

be asked whether the leave can be reinstated. If this is possible, the client should be asked to refund the holiday pay

to the employer. Alternately, the amount may be able to be reimbursed under the Approved Employer scheme.

If the employee refunds the leave payment to the employer, seek written confirmation from the employer detailing:

• the total leave payment the employee is refunding

• the period the leave covers.

NOTE Special case 2: Payment during inability to work

If a payment received during incapacity relates to work carried out in a specific period, the payment should be consi-

dered as earnings in that period.

Example: A real estate agent receives a quarterly commission payment where PAYE is deducted at source. They

suffer an injury on 1 October, and on 14 October receive the commission payment relating to the work they carried out

pre-injury. As this payment is related to work done over a specific period before they became unable to work, it should

not be used in abatement calculations, but instead should be used in the calculation of their earnings before they

became unable to work

Note: This would not apply if the commission payment were received in a later income year. In that case, such a pay-

ment would have to be abated as explained below:

under the Official Information Act 1982

If a payment is related to a period within an income year, but is paid in a later income year, the payment is considered

earnings iable for abatement in that later income year rather than a payment related to the period in the period in the

earlier income year.

This is because subject to the income tax legislation, the Accident Compensation Act 2001, section 9 specifically de-

fines ’earnings as an employee‘ in relation to each income year, which is 1 April to 31 March.

If a payment received while the client is unable to work cannot be related to an equivalent period of time, abatement

should apply only for the week in which the payment was received.

This will be an unusual and rare occurrence, as payments can generally be related to a period of time. Examples

Released

would be:

• a one-off payment paid to an injured worker for accepting a lower paid position

• a taxable bonus payment, such as a profit share or other ‘one-off’ bonus.

ACC must abate these payments if they are received while the client is unable to work. This can disadvantage the

client, particularly if the inability to work is likely to be short-term. In these circumstances, advise the employer that

ACC must abate the client’s weekly compensation in respect of the payment if, received while they are unable to work

and as the inability to work is likely to be short-term, will they consider deferring the payment until after the client’s

weekly compensation has ceased.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 1 of 7

b Holiday pay is to be related to the period in which the holiday leave was actually taken. In some cases, a person may take hol-

iday leave, but not receive holiday pay until much later in the year. If this occurs, the holiday pay should be treated as derived

in the period the leave was taken.

NOTE Example: An employee took holiday leave in June but received payment for that leave in December. The pay-

ment will relate to the actual period that the employee took holiday leave, ie June.

Holiday pay received before the client became unable to work, relating to a period of holiday leave after the date they

became unable to work, is not to be used for their earnings before their inability to work, when calculating weekly

compensation. These earnings may need to be abated.

If a payment is related to a period within an income year, but is paid in a later income year, the payment is considered

earnings liable for abatement in the later income year, rather than a payment related to the period in the earlier income

year.

This is because subject to the income tax legislation, the AC Act 2001, Section 9 specifically defines ‘earnings as an

employee’ in relation to each income year, which is 1 April to 31 March.

2.0 Earnings not liable for abatement

a These payments are not classified as earnings liable for abatement:

• redundancy or superannuation payments paid on or in respect of the termination of employment

• weekly compensation, including payments to a surviving client for an accidental death

• parental leave payments paid under the Parental Leave and Employment Protection Act 1987, Part 7A

• employer top-ups

• payment for work done before they became unable to work.

NOTE Employer top-ups:

If an employee is eligible for weekly compensation following an injury, their employer may make an additional payment

each week that ‘tops up’ the employee’s income during their inability to work to the level of their normal wage, so the

employee has no loss of income.

The ‘top up’ is exempt from the abatement process as long as it:

• does not relate to work performed by the employee

• represents an amount that ‘tops up’ the employee’s weekly compensation to the level of their normal pay.

Note: The employer may need to adjust the employee’s top up amount, if the employee also receives other earnings

that reduces their amount of weekly compensation, eg the employee receives some earnings while they gradually

return to work. Notify the employer of any changes to the weekly compensation rate in these circumstances.

Because ACC normally calculates abatement retrospectively, the employer could already have paid the top-up for the

relevant period. It is possible that by the time ACC calculates the abatement, the top-up amount the employer has

paid, when combined with earnings and weekly compensation, could exceed the client’s normal earnings. The em-

ployer is responsible for adjusting the top-up and recovering any such excess payment.

NOTE Payments for work done before he client became unable to work:

If a client receives earnings that were for work they did before they became eligible for weekly compensation, then

abatement will not apply. Instead they could be included in the calculations that determine the weekly earnings.

Note: If a payment is related to a period within an income year, but is paid in a later income year, then the payment is

considered earning liable for abatement in that later income year, rather than the period in the earlier income year in

which the payments actually relate.

This is because subject to the income tax legislation, the Accident Compensation Act 2001, section 9 specifically de-

fines “earnings as an employee” in relation to each income year, which is 1 April to 31 March.

under the Official Information Act 1982

3.0 When to consider abatement

a For employees:

Any earnings liable for abatement while the client is unable to work due to their injury must be abated against the weekly

compensation payable during that period. Consider abatement for employees if:

• the Real Time Earnings (RTE) portal or ACC003 Employee earnings certificate, giving details of dates and gross amounts

paid, shows that the client has received payments following DOFI/DOSI

• ACC is aware that the client has returned to work and has derived earnings liable for abatement

• the client produces a ‘fit for selected work’ medical certificate.

Released

See Determine employee earnings liable for abatement - Reference.

Determine Employee Earnings Liable for Abatement (CHIPS)

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 2 of 7

b For self-employed and shareholder employees:

Self-employed and non-PAYE shareholder employees only declare actual income to Inland Revenue on an annual basis. How-

ever, during the period the client is unable to work, ACC is required to determine on a week by week basis the amount of earn-

ings liable for abatement that the client is likely to generate from the business or company.

Abatement needs to be considered if the client is either:

• a self-employed person and their business is continuing to operate, or the client starts having input into the business

• a shareholder employee and they continue to work and/or derive earnings from the company.

Note: Unless the self-employed person’s business ceases to function or the shareholder employee ceases to work for the com-

pany, most self-employed or shareholder employees will continue to have some management input, even when they are physi-

cally unable to work.

Indications that abatement should be applied are:

• the ACC004 Questionnaire for self-employed, states that the client’s business or company is continuing to generate income

while they are unable to work or the client has resumed having input into the business or company

• the ACC018 Further medical certificate, states that the client is fit for selected work

• advice has been received in some other way, eg the weekly compensation transcript, that the business or company is contin-

uing to generate income, or that the client is having input into the business or company.

Note: Up until the end of the first income year in which the client became unable to work due to their injury, if the client is self-

employed and is having no involvement with the business while they are unable to work, do not apply abatement. This will

need to be reviewed when the client resumes working in some capacity for the business, or at the end of the income year in

which they became unable to work.

Always make sure that self-employed and shareholder employee clients are aware that weekly compensation is being paid for

loss of earnings, not inability to do some tasks because they are working reduced hours, or to reflect costs of replacement

labour. Any earnings that a self-employed or shareholder employee continues to generate or receive during incapacity must be

abated from weekly compensation.

4.0 Methods of determining earnings while unable to work

a Self-employed and shareholder employees:

A self-employed or shareholder employee’s actual earnings for a period cannot be established until the end of an income year.

However, Clause 50 of Schedule 1 allows ACC to estimate earnings for a period where the actual earnings cannot be ascer-

tained.

ACC has developed two approaches, depending on whether:

• earnings were generated during a period when the client was unable to work that occurred in part of an income year

• earnings were generated over a full income year.

b Inability to work for part of an income year:

A claim will always begin partway through an income year, unless the client becomes unable to work on 1 April (or the day their

income year started, if the client has a non-standard balance date).

In these cases, ACC makes an estimate of the client’s earnings liable for abatement during the period the client is unable to

work, based on information about he level of work that the client is able to do. This estimate stands as final assessment,

unless fraud is subsequently established.

An estimate is required because actual earnings for the part year period that the client was unable to work cannot be deter-

mined. That is, when the client declares their actual income to Inland Revenue, they will declare a sum that represents their

under the Official Information Act 1982

earnings over the whole income year. From this figure, there is no way to accurately determine how much of the income de-

clared in that income year was earned:

• before they became unable to work

• while they were unable to work

• after they became able to work again.

Note: Some clients will be able to provide details of actual earnings while they were unable to work by supplying accounts for

actual income less expenditure. The details can then be used to estimate the earnings liable for abatement. Before using these

accounts, consider whether a referral to the ACC accounting advisor is necessary.

c Inability to work for a full income year:

Released

If the client is unable to work for a full income year:

• an interim estimate of earnings while they were unable to work must be completed

• an end of year adjustment is required, based on the actual earnings for that year, as lodged with Inland Revenue.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 3 of 7

NOTE For example, a client becomes unable to work due to their injury from 4 July 2001 until 11 November 2003

would have their earnings when they become able to work again determined as follows:

• 4 July 2001 to 31 March 2002

— Part income year

— Estimate earnings while unable to work

• 1 April 2002 to 31 March 2003

— Full income year

— Interim estimate subject to a final adjustment, based on actual earnings as declared to Inland Revenue for the full

income year

• 1 April 2003 to 11 November 2003

— Part income year

— Interim estimate with a final adjustment at the end of the period they were unable to work, if required.

d Estimating earnings while unable to work due to the injury:

Estimates of earnings while the client is unable to work can be based on one of the following:

• a comparison of hours worked before and after the period they were unable to work. See Compare hours worked

• a negotiated percentage that estimates the earning capacity of the client. See Negotiate percentage earning capacity or earn-

ings amount

• an estimate of the income that the client would receive during the period they are unable to work. See Assess earnings for

the first income year.

Note: For the first income year, abatement based on an estimate can apply as a final assessment, ie there is no need to make

an adjustment based on the income return lodged with Inland Revenue, because actual earnings during that part year cannot

be determined.

If at the start of an income year, an interim estimate is applied, the risk of overpayment can be reduced by making low pay-

ments until the end of a full income year, then making an adjustment based on actual earnings lodged with Inland Revenue for

the full income year.

e Self-employed and shareholder employees:

For self-employed and shareholder employees the following factors should be considered when estimating earnings while the

client is unable to work due to their injury.

For self-employed consider:

• the effect on the business income of their inability to work

• the cost of replacement labour and the effect of this on the profitability of the business

• if there has been a significant downturn or upturn in the business, eg an apple grower who is facing reduced returns due to

low prices on the export crops

• any other issues relevant to the particular business

For shareholder employees consider:

• the amount of work that the shareholder continued to do for the company, including management duties, and the likely

remuneration for that work

• any actual earnings the client continues to receive from the company need to be abated. Payments made by the company in

the form of wages or salary are actual earnings and must be abated

• there may be a need to estimate additional income that the client may receive at a later time, such as director’s fees

• the influence that a shareholder employee has over the income awarded by the company

Compare Hours Worked (CHIPS)

Negotiate Percentage Earning Capacity or Earnings Amount (CHIPS)

under the Official Information Act 1982

Determine Earnings if No Agreement (CHIPS)

Assess Earnings for the First Income Year (CHIPS)

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 4 of 7

5.0 What to do at the start of a new income year

a Overpayments can arise if payments made during the year are higher than the final amount the client is eligible for. To manage

this risk one month before the start of a new income year, ACC sends self-employed and shareholder employee clients an on-

going claims letter WC004 Self-employed and shareholder employee abatement election which:

• advises clients of the basis of payments for the following income year

• requests that they elect how payments should be made.

This is required because if the client is unable to work due to the injury for a full income year, an adjustment to the abatement

assessment is made, based on the earnings lodged with Inland Revenue at the end of that income year.

The election should aim to reflect the true level of anticipated earnings. It should be conservative to the extent that it will mini-

mise the risk of an overpayment. However, not conservative to the extent that ACC are withholding weekly compensation

having regard to the client’s likely payment amounts at the end of the income year.

On the election, the client can request one of the following:

• earnings during the new income year continue to be based on an estimated method, and the client will accept the risk that an

overpayment may arise if unable to work for the full year

• payments stop in the meantime until actual earnings are lodged with Inland Revenue

• ACC contact them to discuss ways to reduce the risk of overpayment.

When the election is returned, the method for estimated payments for the coming income year is set up.

Note: The client still has to supply regular medical certificates, provide details of any changes in their input into the business or

company during their inability to work and comply with their rehabilitation programme.

6.0 Reassessing earnings at the end of a full income year

a For a full income year, the client will have received the rate of compensation that they elected at the start of that income year

or an assessment of the amount to be abated pending end of year accounts. An adjustment is required to the end of year, or to

the end of their eligibility for weekly compensation, for each complete income year that the client is unable to work.

b Validating accounts for earnings while unable to work

Be aware that it is possible for the client to make changes in accounting practice after the injury to reduce their earnings while

they are unable to work. Common examples of this are:

• charging interest on partners’ current accounts where this has not been done previously

• payment of wages to family members. Check that this reasonably reflects tasks undertaken that were previously actioned by

a client

• payment of management fees to other entities or other partners

• change in policy for allocating partnership profits or shareholder salary. In order to identify such a change, partnership or

company financial statements are required, because the ACC176 Earnings certificate – Inland Revenue and IPS2 do not con-

tain sufficient detail to determine whether or not this has occurred.

ACC176 Earnings certificate - Inland Revenue

c Accounting Advisory Service referrals

If you're unsure of the validity of information about the client’s business or company or the client’s financial circumstances are

complicated, consider referring to the Technical Accounting Specialists for advice (see link below).

d What to do if client ceases to be unable to work

Where a claim is in the Actioned Queue and a reassessment is necessary a Team Manager or Team Leader from the Weekly

Compensation team may change the LPL indicator to ‘No’ to allow Pathway to be accessed.

under the Official Information Act 1982

• The request and approval to Activate will be confirmed by use of the most appropriate task in Eos

• The indicator wil be changed to ‘yes’ after the wash-up is completed.

If the client fully returns to work part-way through the income year, and actual earnings for that period of inability to work can

not be readily established, then the estimated earnings figure while they were unable to work can be used as a final abatement

assessment.

If the client had elected to continue receiving weekly compensation based on estimated earnings while they are unable to

work, and this has been updated whenever the client’s circumstances change, then there is no need for an adjustment.

If the client elected to receive a lower rate or full rate of payment during the income year:

Released

• an adjustment will be required

• arrears may need to be paid or overpayment may need to be recovered.

Note: The client should have been providing regular declarations on the ACC206 Self-employed work hours declaration form of

their involvement with the business or company during the income year.

ACC206 Self-employed Work Hours Declaration Form (CHIPS)

PROCESS

Referring to the Technical Accounting Specialists for Advice

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 5 of 7

7.0 Special Case: Considering earnings derived in overseas currency

a The Accident Compensation Act 2001, Schedule 1, Clauses 49(4) and 49(5) allow ACC to apply abatement to earnings that a

client derives in overseas currency.

In some cases, long-term clients have moved overseas and continue to receive weekly compensation. When this applies, if the

client starts working and/or deriving income overseas, that income is earnings liable for abatement, which is applied in the

abatement formula and may reduce the amount of weekly compensation payable.

See Pay client overseas for information about eligibility to receive weekly compensation overseas and the client’s obligations

while living outside NZ.

Eligibility for Weekly Compensation while Client is Overseas Policy

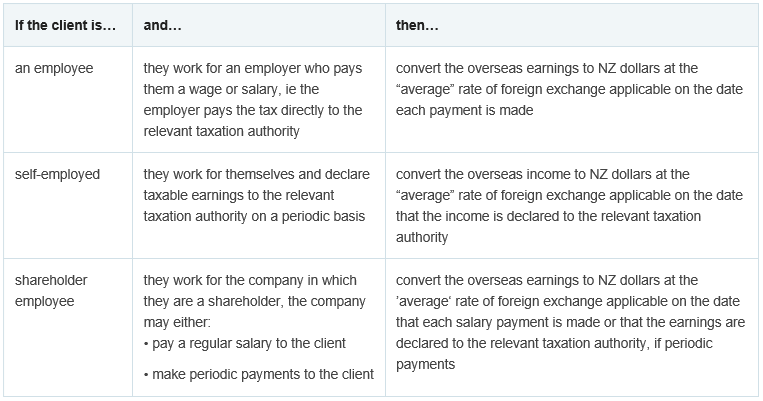

b ACC is required to convert the overseas income into NZ dollars at an average rate of foreign exchange applied for the date

that the payment is made. To determine the average rate of foreign exchange for a particular currency, ACC uses the following

indices:

• If the currency is AUST, UK, USA, YEN, EURO then use the conversion rates published by the Reserve Bank on NZ on the

following web site: www.rbnz.govt.nz/statistics/exandint/b1/data.html

• If the currency is not AUST, UK, USA, YEN, EURO, or NZ then use the conversion rates published by the Customs Service

on the following web site: www.customs.govt.nz/news/utilities/Pages/Rates-Of-Exchange.aspx

The overseas earnings must be converted to NZ dollars at the rate of foreign exchange applicable for the period or the date on

which the payment was made.

Reserve Bank on NZ

http://www.rbnz.govt.nz/statistics/exandint/b1/data.html

NZ Customs Service

http://www.customs.govt.nz/news/utilities/Pages/Rates-Of-Exchange.aspx

c When considering the abatement of overseas earnings, decide which earnings category the overseas income falls into:

• earnings as an employee

• earnings as a self-employed person

• earnings as a shareholder employee.

This classification will affect how abatement is applied and the dates of payment for when the overseas currency is converted

to NZ dollars.

• If the client is an employee and they work for an employer who pays them a wage or salary (ie the employer pays the tax di-

rectly to the relevant taxation authority), then convert the overseas earnings to NZ dollars at the “average” rate of foreign ex-

change applicable on the date each payment is made.

• If the client is self-employed and they work fo themselves and declare taxable earnings to the relevant taxation authority on

a periodic basis, then convert the overseas income to NZ dollars at the “average” rate of foreign exchange applicable on the

date that the income is declared to the relevant taxation authority.

• If the client is shareholder employee and they work for the company in which they are a shareholder, the company may

either:

— pay a regular salary to the client

— make periodic payments to the client

then convert the overseas earnings to NZ dollars at the ’average‘ rate of foreign exchange applicable on the date that each

salary payment is made, or that the earnings are declared to the relevant taxation authority if periodic payments.

under the Official Information Act 1982

Abate Overseas Earnings (CHIPS)

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 6 of 7

Dates of payment for when overseas currency is converted to NZ dollars.PNG

8.0 Links to legislation

Accident Compensation Act 2001, section 9 - earnings as an employee

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100608.html

Accident Compensation Act 2001, Schedule 1, Clause 49 - earnings definitions

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104895.html

Accident Compensation Act 2001, Schedule 1, Clause 50 - estimation for abatement purposes of eanrings that cannot be

ascertained

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM105401.html

under the Official Information Act 1982

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Abatement > Determine Earnings Liable for Abatement

Uncontrolled Copy Only : Version 8.0 : Last Edited Wednesday, 6 November 2019 9:14 AM : Printed Tuesday, 4 August 2020 7:29 PM

Page 7 of 7

Earners' Account (Non-Work) Fund Policy v4.0

Summary

Objective

Earners' Account (Non-Work) Fund Policy v4.0

Summary

Objective

Use this guidance to help you ensure that claims made by earners, but that are non-work injuries, are funded accurately. This page

informs you about how the Earners’ Account is funded, and what it covers.

1) Rules

2) Other criteria for funding from the Earners' Account

3) Link to Legislation

Background

An earner is a person who is in employment for financial gain or profit as an employee, a self-employed person or a shareholder em-

ployee.

The Earners’ Account is funded from levies paid by all earners, regardless of whether they are employees or self-employed.

The Earners’ Account funds support for non-work injuries suffered on or after 1 July 1992, by people who have some paid employ-

ment (except motor vehicle and treatment injury accidents).

Owner

Martin Shelton

Expert

Deborah Doroshuk

Policy

1.0 Rules

a The Earners’ Account is funded from levies paid by all earners, regardless of whether they are employees or self-employed.

Fund code: earners (non-work)

2.0 Other criteria for funding from Earners’ Account

a Earners may include people who:

• are on unpaid leave

• have recently stopped working as an employee

• are in casual or seasonal work

• have purchased Earner status, e.g. TimeOut cover

• are receiving weekly compensation.

Clients who have finished work before they are injured can be considered an employee at date of injury if they either:

• received holiday pay and become unable to work due to the injury during the period covered by the holiday pay

• become unable to work within 28 days of finishing work and would have been in employment within three months of the date

of their injury.

•they meet specific rules and criteria to be considered as seasonal workers

NOTE The holiday leave period and the 28-day period are not added together.

under the Official Information Act 1982

The holiday leave period and the 28-day period are not added together. Only one period can be applied. People in this

situation have ‘extended earner’ status. See example below, or they meet specific rules and criteria to be considered

as seasonal workers.

NOTE Example of ‘extended earner’ status:

An employee leaves their job on 10 August 2010 and is due to start a new job on 1 October 2010. They are paid two

weeks’ holiday pay. They slip and suffer a leg injury on 31 August.

• The injury occurred fewer than 28 days after they finished work and they are due to start their new job within three

months

• We can attribute claim costs to the Earners’ Account because their employee status is extended.

Released

3.0 Link to Legislation

Accident Compensation Act 2001, Section 218, Earners’ Account: Application and source of funds

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM102831.html

ACC > Claims Management > Manage Claim Registration and Cover Decision > Operational Policies > Fund Code > Earners' Account (Non-Work) Fund Policy

Uncontrolled Copy Only : Version 4.0 : Last Edited Wednesday, 18 December 2019 3:28 PM : Printed Tuesday, 4 August 2020 7:31 PM

Page 1 of 1

Eligibility Criteria for Weekly Compensation v11.0

Summary

Objective

Eligibility Criteria for Weekly Compensation v11.0

Summary

Objective

Use this guidance to help you determine whether a client is eligible for weekly compensation from ACC under the Accident Compen-

sation Act 2001. This policy applies to claims where the client became unable to work from 1 July 2010.

1) Eligibility criteria

2) Section 103 - Can the client do the job they were doing before they were injured?

3) Section 105

4) Extension of Earner Status

5) Eligibility

6) Review inability status periodically

7) Termination of an employment

8) Links to legislation

Owner

Martin Shelton

Expert

Deborah Doroshuk

Procedure

1.0 Eligibility criteria

a For a client to be eligible for weekly compensation from ACC, all the following criteria must be met:

• the claim for personal injury is accepted for cover under the Accident Compensation Act 2001, and

• ACC is responsible for managing the claim (that is, it is not a work-related personal injury suffered by an employee of an

accredited employer), and

• the client has made a written or verbal application for weekly compensation, and

• the client is unable to work because of the personal injury under either section 103 or section 105.

2.0 Section 103 - can the client do the job they were doing before they were injured?

a Under section 103 of the Accident Compensation Act 2001, ACC must determine a client’s inability to work – and therefore

their eligibility to weekly compensation – by determin ng whether they could do the job they were doing before they were in-

jured.

b The people who are eligible for weekly compensation include those who, at the time they suffered their personal injury, were:

• in employment and had earnings immediately prior to becoming unable to work as one or more of an employee, self-

employed and shareholder employee; or

• on unpaid parental leave; or

• a recuperating organ donor and receiving payments under the Compensation for Live Organ Donors Act 2016; or

• in consecutive periods of unpaid parental leave and a payment period under the Compensation for Live Organ Donors Act

2016.

c In all cases, the client must have earnings immediately prior to becoming unable to work as one or more of an employee, self-

employed and shareholder employee.

under the Official Information Act 1982

NOTE What if they are on unpaid parental leave?

Clients on unpaid parental leave at the time of their injury are deemed to be in employment for the purposes of Sec-

tion 103.

NOTE What if clients are receiving organ donor compensation?

Clients who are recuperating organ donors under the Live Organ Donors Act 2016 are deemed to be earners if they:

• are injured during a payment period under that Act which was immediately preceded by a period of employment in

which they were receiving earnings. Their inability to work is tested under section 103; or

• are injured during consecutive periods of unpaid parental leave and a payment period under the Live Organ Donors

Act 2016. Their inability to work is tested under section 103; or

• had no earnings immediately prior to the organ donor payment period, they meet the timeframes under clause 43 of

Released

Schedule 1 at the commencement of the payment period. Their inability to work is tested under section 105.

3.0 Section 105

a We can’t determine inability to work under section 103 for those clients who:

• have an extension of earner status under clause 43 of Schedule 1

• are a potential earner (LOPE) at the time he suffered his injury, they may be eligible for loss of potential earnings

• have purchased weekly compensation under section 223.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Eligibility Criteria for Weekly Compensation

Uncontrolled Copy Only : Version 11.0 : Last Edited Tuesday, 10 December 2019 5:24 PM : Printed Tuesday, 4 August 2020 7:32 PM

Page 1 of 2

4.0 Extension of earner status

a Clients may have an extension of earner status under clause 43 of Schedule 1 because:

• leave payments that are liable for earner levy on ceasing employment extend the period of employment up to or beyond the

date they became unable to work, or

• they became unable to work within 28 days after ceasing employment as an employee and had an employee job to return to

within 3 months, or

• they became unable to work within 28 days after ceasing seasonal employment as an employee where they had been em-

ployed in the two previous seasons and the employer confirms that the client could reasonably expect to have been employed

again within 12 months, or

• they became unable to work during a payment period under the Live Organ Donor Compensation Act 2016 and they sat sfy

the timeframes under clause 43 of Schedule 1 at the start of that payment period (as if that was the date they were unable to

work).

b Please ask the client to sign the ACC165 Declaration of rights and responsibilities form, as described in the method for the ini-

tial interview, declaring that they understand their responsibilities for receiving weekly compensation.

ACC165 Declaration of rights and responsibilites

5.0 Eligibility

a The rules for determining the level and duration of support are driven by:

• the dates when a client initially and/or subsequently became unable to work in the employment they held at that date (date of

first incapacity 'DOFI', or date of subsequent incapacity 'DOSI')

• confirmation of ongoing inability to work.

b Refer to links below for additional information.

Definition of Incapacity

Determine incapacity dates – date of first incapacity (DOFI) (CHIPS)

Determine if a subsequent incapacity (CHIPS)

6.0 Review inability status periodically

a When a client is eligible for weekly compensation it is important to continue to periodically review their inability to work.

b See the link below for additional information.

Determine incapacity under section 103

http://thesauce/team-spaces/chips/compensation/weekly-compensation/reference/incapacity-187/determine-incapacity-

under-s103/index.htm

Determine incapacity under section 105

http://thesauce/team-spaces/chips/compensation/weekly-compensation/reference/incapacity-187/determine-incapacity-

under-s105/index.htm

7.0 Termination of an employment

under the Official Information Act 1982

a If the employment a client held at DOFI/DOSI is terminated during the period that they are unable to work, they are still eligible

for weekly compensation so long as they continue to be unable to work.

8.0 Links to legislation

Accident Compensation Act 2001, section 103

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM101458.html?search=ts_act%40bill%40regulation%

40deemedreg_Accident+COmpensation+Act_resel_25_a&p=1

Accident Compensation Act 2001, section 105

Released

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM101462.html?search=ts_act%40bill%40regulation%

40deemedreg_Accident+COmpensation+Act_resel_25_a&p=1

Accident Compensation Act 2001, Schedule 1, Clause 43, Weekly earnings if employment ended before commencement

of incapacity

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104879.html?search=ts_act%40bill%40regulation%

40deemedreg_Accident+COmpensation+Act_resel_25_a&p=1

Compensation for Live Organ Donors Act 2016

http://www.legislation.govt.nz/act/public/2016/0096/latest/DLM4297829.html?src=qs

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Eligibility Criteria for Weekly Compensation

Uncontrolled Copy Only : Version 11.0 : Last Edited Tuesday, 10 December 2019 5:24 PM : Printed Tuesday, 4 August 2020 7:32 PM

Page 2 of 2

Eligibility for Weekly Compensation while Client is Over-

Eligibility for Weekly Compensation while Client is Over-

seas Policy v9.0

Summary

Objective

Refer to this guidance to help you determine whether a client is eligible to receive weekly compensation while overseas, and how to

manage ongoing eligibility for weekly compensation.

1) Personal injury within New Zealand

2) Personal injury outside New Zealand

3) Medical certification by overseas medical/nurse practitioner

4) Taxation of weekly compensation paid to Australian residents

5) Determine eligibility for weekly compensation if injured overseas

6) Overseas income and weekly compensation

7) Criteria for earner in receipt of New Zealand taxable earnings at DOFI

Owner

Tui Kailahi

Expert

Nick Lamb

Policy

1.0 Personal injury within New Zealand

a Both the following points apply for the period they are outside New Zealand:

• they must provide ACC with ongoing medical confirmation that they are unable to work due to the injury

• ACC must approve the doctor/nurse practitioner providing that medical certificate

If weekly earnings were based on earnings from illegal employment, eg working without a work permit, then:

• a reassessment is required, to remove the illegal earnings from the weekly compensation calculation.

This is effective for the period the client is outside New Zealand

2.0 Personal injury outside New Zealand

a Section 127 of the Accident Compensation Act 2001 (AC Act 2001) outlines the criteria for the payment of weekly compen-

sation to a client while they are overseas.

Section 127, AC Act 2001 - Payment of weekly compensation and lump sum compensation to claimant outside New Zeal-

and

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM101806.html

b Clients who have sustained personal injury while overseas, and who are living outside New Zealand, are eligible for weekly

compensation in limited circumstances, which are described below:

• the general eligibility rules apply, i.e. they must be an earner with New Zealand taxable earnings at the date they became

unable to work due to the injury

• a client may be eligible for consideration if they had earnings within the six-month period prior to leaving New Zealand, but

they must still meet the first criterion, above

• they must provide ACC with satisfactory medical confirmation of their inability to work.

under the Official Information Act 1982

This also applies when establishing weekly compensation payable on a fatal claim, if the deceased client was overseas at the

date of death

Go to Accidental Death Support Policy.

Accidental Death Support Policy

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Payments > Eligibility for Weekly Compensation while Client is

Overseas Policy

Uncontrolled Copy Only : Version 9.0 : Last Edited Monday, 21 October 2019 4:33 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 1 of 3

3.0 Medical certification by overseas medical/nurse practitioner

a Special criteria apply for accepting medical certificates for the client becoming unable to work while overseas, in both the fol-

lowing instances:

• a client is injured in New Zealand and goes overseas

• a client sustains an injury overseas that has cover

If the client is overseas and provides medical certificates for inability to work from an overseas doctor or nurse practitioner,

these can be accepted if the:

• medical certificate clearly states the limitations the client is experiencing

• medical certificate states the period that the client is unable to work as a result of these limitations, up to a maximum of 13

weeks

• doctor or nurse practitioner has provided sufficient details of their qualifications and these qualifications are comparable to

registered medical or nurse practitioners, who are able to practice in New Zealand

• medical certificate is written in English.

A decision on acceptability can then be made taking into consideration qualifications of the practitioner, the nature of the injury,

and the limitations being experienced in relation to the client’s pre-injury employment.

4.0 Taxation of weekly compensation paid to Australian residents

a A person is considered a tax-resident in Australia if they live there for more than six months a year. Any other clients who are

about to move to Australia must be advised of these new tax rules, and instructed to contact the Inland Revenue Department

(IRD) and the Australian Tax Office (ATO) about their tax liability.

It can be difficult to identify clients who are Australian residents as we do not explicitly identify clients by country. A report has

been generated of all clients who are currently receiving weekly compensation, and searched for some derivative of ‘Australia’

in their postal, residential or case payee addresses.

b The IRD and the ATO have agreed that weekly compensation for Australian residents will no longer be taxed in New Zealand

but in Australia.

c These clients must approach the ATO to seek information about their tax liab lity in Australia. For people who have been living

there and receiving weekly compensation for a number of years, it is likely that the ATO will seek back-taxes from them for the

entire period of their residency in Australia. These clients will also need to contact IRD to discuss any tax refunds for those

years.

ACC has no jurisdiction in this matter, and is required by law to implement these changes. We cannot enter into any discussion

about the tax treatment of these payments, and anyone enquiring about this needs to be directed to either the Australian Tax

Office or the Inland Revenue Department.

The contact details for IRD and the ATO are:

• Inland Revenue Department (calling from overseas) on +64 4 978-0779

• Australian Tax Office (calling from Australia) on 13 28 61.

5.0 Determine eligibility for weekly compensation if injured overseas

a A client may have cover through ACC for an injury that occurred overseas, because they were ordinarily resident in New Zeal-

and at the time.

The following criteria must be met for a client to be eligible for weekly compensation in these circumstances:

• the client must be an earner receiving New Zealand taxable earnings as at start of the period they were unable to work due to

the injury

• ACC must be satisfied that the client is unable to work due to the injury. See Determine if medical certificate completed over-

seas is acceptable.

Determining if Medical Certificate Completed Overseas is Acceptable (CHIPS)

under the Official Information Act 1982

6.0 Overseas income and weekly compensation

a 7. Overseas income and weekly compensation

When a pe son has earned overseas income before becoming unable to work due to the injury, it is possible that some or all of

this income can be included in the calculation of their weekly compensation. The following should be considered:

• In all cases, they must be a New Zealand tax resident to have their income considered for ACC purposes

• If the person is employed overseas and paid PAYE deducted salary or wages by a New Zealand based employer, and the

employer declares the wages to IRD, these will be considered ‘earnings as an employee’.

• If the person works overseas for an overseas company, the earnings they receive may be classed as self-employed earnings,

Released

and would need to be declared on an IR3 as ‘Overseas Income’. Regardless of whether the person is classed as an employee,

the earnings would not meet the definition of ‘earnings as an employee’ as defined in section 9 of the Accident Compensation

Act 2001.

• Earnings declared as ‘overseas income’ still may not have been billed ACC levies. Any claim with overseas income should be

referred to the Technical Accounting Specialists to determine how much of the income is relevant for ACC’s purposes.

Accident Compensation Act 2001, section 9: Earnings as an employee

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM100608.html

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Payments > Eligibility for Weekly Compensation while Client is

Overseas Policy

Uncontrolled Copy Only : Version 9.0 : Last Edited Monday, 21 October 2019 4:33 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 2 of 3

7.0 Criteria for earner in receipt of New Zealand taxable earnings at DOFI

a ACC needs to determine whether the client can be classified as an earner, in receipt of New Zealand taxable earnings, at the

start of the period they became unable to work.

b The following categories of client could meet the criteria:

• working overseas and receiving New Zealand taxable earnings

• overseas on a brief period of unpaid leave (see the guidance ‘Deciding eligibility and employment’ linked below)

• eligible under of AC Act 2001, Schedule 1 Clause 43, i.e. overseas on leave and received holiday pay before they left (see

the guidance ‘Extension of employee status’ linked below)

• eligible under AC Act 2001, Schedule 1 Clause 44, i.e. they are on a period of unpaid parental leave

• eligible under AC Act 2001, Section 223 (see guidance ‘Purchased TimeOut cover’ linked below)

• eligible under AC Act 2001, Schedule 1 Clause 47 and have received earnings in the six months before leaving NZ. Go to

Loss of Potential Earnings (LOPE) to determine, gather information and calculate loss of potential earning capacity (LOPE)

Deciding Employment Type and Eligibility (CHIPS)

Purchased TimeOut Cover

Loss of Potential Earnings (LOPE)

Section 223 Persons eligible to purchase weekly compensation

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM102844.html

Schedule 1, Clause 43 Weekly earnings if employment ended before commencement of incapacity

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104879.html

Schedule 1, Clause 44 Weekly earnings if employee on unpaid parental leave immediately before his or her incapacity

commenced

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104883.html

Schedule 1, Clause 47 Corporation to pay weekly compensation for loss of potential earnings capacity

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104891.html

under the Official Information Act 1982

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Payments > Eligibility for Weekly Compensation while Client is

Overseas Policy

Uncontrolled Copy Only : Version 9.0 : Last Edited Monday, 21 October 2019 4:33 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 3 of 3

Extension of Employment Status v8.0

Summary

Objective

Extension of Employment Status v8.0

Summary

Objective

Refer to this guidance to help you determine when extension of employment status applies. This guidance applies to claims where

the client became unable to work from 1 July 2010.

1) When to consider extension of employment status

2) Confirm employment has ceased

3) Required information to confirm cessation for self or shareholder employment

4) Extension of employment status applies

5) Eligibility criteria

6) Situations where the client had ‘arranged’ to enter an employment agreement

7) Criteria for extension: termination pay

8) Criteria for extension: employee job to go to

9) Seasonal workers

10) Level of proof: employee job to go to

Owner

Martin Shelton

Expert

Deborah Doroshuk

Policy

1.0 When to consider extension of employment status

a Consider a client’s eligibility for extension of employment status under the Accident Compensation Act 2001, Schedule 1

Clause 43, if all the following apply:

• they are unable to work due to the injury

• the date they first or subsequently became unable to work (date of first incapacity 'DOFI' or date of subsequent incapacity

'DOSI') is after the date that the client recently ceased employment as either:

— an employee

— a self-employed person

— a shareholder employee

• they do not otherwise have employment.

2.0 Confirm employment has ceased

a For clients who were employees before they became unable to work, confirm the date their employment was terminated with

their last employer.

b For clients who were either self-employed or shareholder employees before they became unable to work, as these clients

were their own employers, determining the date that employment ceases requires more information.

3.0 Required information to confirm cessation of self or shareholder employment

a ACC can generally accept that self-employment or shareholder employment has ceased from the date the last of the following

under the Official Information Act 1982

activities is carried out, including:

• the date the client’s business ceased to trade

• the date the client fulfilled the business tax obligations required by Inland Revenue when, ceasing to operate a business, e.g.

completing a business cessation form, cancelling employer registration, cancelling GST registration, and filing a final tax return

• the date their accountant confirms the client has ceased their employment

• the date the premises used for carrying out the business has either been sold or a lease has expired or been terminated

Released

• the date when assets essential for the continuation of the business have been disposed of

• the date when services previously used by the business, such as telephone, bank accounts, insurances and power, have

been discontinued

• the date of bankruptcy of a self-employed person or the date the company of a shareholder employee, has been struck off

the Companies Register, if applicable.

b If further clarification is required to determine if a client’s self-employment or shareholder employment has ceased, please con-

tact the Technical Accounting Services team.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Extension of Employment Status

Uncontrolled Copy Only : Version 8.0 : Last Edited Tuesday, 28 January 2020 3:25 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 1 of 5

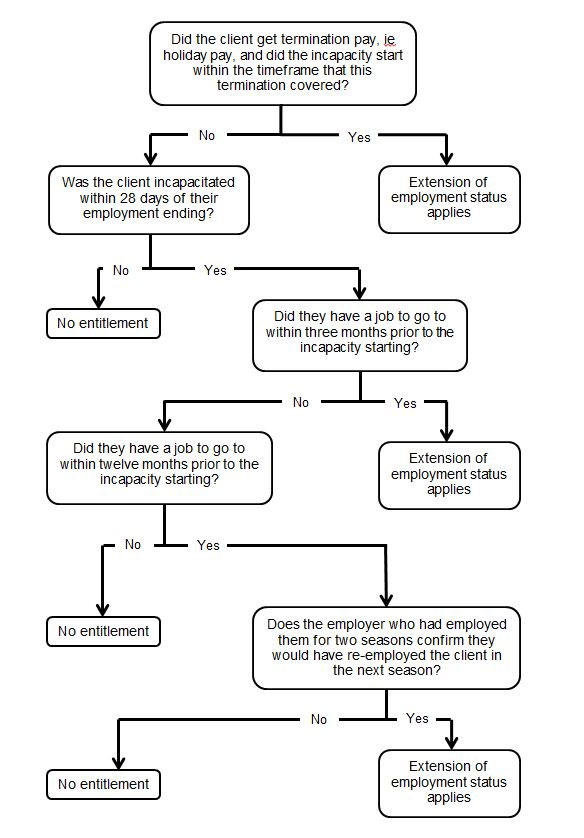

4.0 Extension of employment status

a

4.0 Extension of employment status

a Use the flowchart attached to help determine when extension of employment status applies.

under the Official Information Act 1982

Released

Does extension of employment status.jpg

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Extension of Employment Status

Uncontrolled Copy Only : Version 8.0 : Last Edited Tuesday, 28 January 2020 3:25 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 2 of 5

5.0 Eligibility criteria

a A client can have extended employment status if, at DOFI/DOSI, they had recently stopped work, and fit one of the following

scenarios:

• they received a termination payment on ceasing employment that equates to a certain number of days pay; this number of

days is added to their employment cease date and they become unable to work within this extended period

• they become unable to work due to the injury within 28 days of ceasing employment and if it were not for the inability to work,

they would have been employed as an employee within either:

— three months after the date they became unable to work, had entered an employment agreement or had arranged to enter

an employment agreement before they became unable to work

— twelve months after the date they became unable to work, if the client is a seasonal worker and the employer, who must

have employed the client for the last two seasons, confirms there is a reasonable expectation they would have re-employed

the client in the next season.

The business rule below defines the Extension of Earner Criteria.

Extension of earner status criteria

Determine extension - termination pay - Reference

http://thesauce/team-spaces/chips/compensation/weekly-compensation/reference/eligibility-187/determine-extension---

termination-pay/index.htm

b When considering Accident Compensation Act 2001, Schedule 1 Clause 43:

• the above scenarios run concurrently, not consecutively. That is, consider the 28 days in scenario 2 as running from the last

day of employment, not from any extended date due to termination pay

• the extension due to termination pay, runs from the day the employment ceased

• the period that the client has been employed prior to DOFI/DOSI is not relevant in determining if the extension applies.

See ‘Determine extension - employee job to go to' below.

Accident Compensation Act 2001, Schedule 1 Clause 43

http://www.legislation.govt.nz/act/public/2001/0049/latest/DLM104879.html

Determine extension - employee job to go to - Reference

http://thesauce/team-spaces/chips/compensation/weekly-compensation/reference/eligibility-187/determine-extension---

employee-job-to-go-to/index.htm

6.0 Situations where the client had ‘arranged’ to enter into an employment agreement

a Under the Accident Compensation Act 2001, Schedule 1 Clause 43(3)(a), extension of earner status can apply if a client had

entered into an employment agreement, or had arranged to enter an employment agreement, before the client became unable

to work due to the injury (i.e. something short of an employment agreement, but also something more than a mere hope of

employment).

NOTE Example

If an employer advises that a client was 'on my staffing list awaiting a vacancy', ACC would need to seek further clari-

fication of what the staffing list entailed. If this was simply a list used for replacements once a current employee re-

signed, this could be considered insufficient to constitute 'an arrangement to enter into an employment agreement'.

under the Official Information Act 1982

However if the employer advised the list was used to take on workers as work became available and it is clear the

work due to its nature would become available, and the client would have been hired in the immediate future, then this

could constitute an 'arrangement to enter into an employment agreement'.

b Ultimately the question that needs to be satisfied is whether at the date the client became unable to work due to the injury, the

arrangement in place meant it was more likely than not that they would have been in employment in the immediate future.

c If there are doubts about a client’s eligibility when they have 'arranged to enter into an employment agreement', a compre-

hensive referral can be completed and forwarded to the Weekly Compensation Panel. See the below link for the referral

process to the Weekly Compensation Panel.

Technical Services Panels

Released

http://thesauce/team-spaces/technical-services-ts/technical-policy/panels/index.htm

7.0 Criteria for extension: termination pay

a If a client received a payment of earnings on which an earner levy is payable (such as holiday pay) upon ceasing work as an

employee, they are considered to be an earner for the equivalent number of days to which the payment relates.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Extension of Employment Status

Uncontrolled Copy Only : Version 8.0 : Last Edited Tuesday, 28 January 2020 3:25 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 3 of 5

NOTE Example

If a person is paid 10 days’ holiday pay upon termination, they continue to be classified as an employee for 10 working

days after the actual date they finished work. In this situation, if they became unable to work due to the injury within

those 10 working days of ceasing employment, they are eligible for weekly compensation under this category.

When considering the number of days pay, have regard to the person’s work pattern. For example, 10 days holiday

pay for a 3 day per week worker would extend the person status as an employee by 3 weeks and 1 day.

8.0 Criteria for extension: Employee job to go to

a The client is eligible for weekly compensation if all the following criteria are met:

• they become unable to work due to the injury within 28 days of ceasing employment either as an employee, a self-employed

person or a shareholder employee, and

• if it was not for the inability to work, they would have been employed as an employee within:

— three months after the date they became unable to work and had entered an employment agreement or had arranged to

enter an employment agreement before they became unable to work

— twelve months after the date they became unable to work, if the client is a seasonal worker and the employer (who must

have employed the client for the last two seasons, over the last two years) confirms that there is a reasonable expectation that

they would have re-employed the client in the next season.

b The prospective employer is required to complete a ACC685 Prospective employer declaration.

ACC685 Prospective employer declaration

9.0 Seasonal workers

a A seasonal worker is an employee:

• whose employment is governed by the availability of work, and

•there is an understanding between the employer and employee that the employment will terminate when the work is no longer

available.

To meet this definition of a seasonal worker, the client must demonstrate that they have worked for the employer for at least

the last two seasons over the last two years.

NOTE Examples

A person is employed as an apple picker on the understanding that the work will terminate for that season when there

are no more apples to be picked; therefore, hey are a seasonal worker.

A university student is employed in a supermarket for each holiday period, and the work terminates when the student

returns to university. This is not considered to be seasonal employment as the availability of work continues despite

the fact that the student is not available to work.

b Typical types of seasonal workers include:

• shearers

• freezing workers

• floriculture workers

• horticulture workers

• ski industry workers.

c This is not an exhaustive list. If unsure if a client is a seasonal worker, contact a Technical Specialist.

under the Official Information Act 1982

10.0 Level of proof: employee job to go to

a If a client is injured within 28 days of ceasing employment, ACC will accept that a client is eligible for weekly compensation, if

either of the following applies:

• They will be employed as an employee within 3 months of the date they became unable to work due to the injury, and had en-

tered an employment agreement or had arranged to enter the employment agreement before they became unable to work,

and the prospective employer confirms in writing the date the arrangement was made and the expected start date.

Released

• They will be employed as an employee within 12 months (for seasonal workers) and the employer confirms in writing that

they have employed the client for the last two consecutive seasons and would, if not for the inability to work, be likely to re-

employ the client for the next season.

b The prospective employer must be a valid employer registered with Inland Revenue and ACC for the purposes of paying PAYE

tax and employer levy respectively. Use the employer search on Pathway to establish if an employer is registered with ACC.

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Extension of Employment Status

Uncontrolled Copy Only : Version 8.0 : Last Edited Tuesday, 28 January 2020 3:25 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 4 of 5

NOTE Example 1

A hardware shop assistant ceases employment as an employee on 20 May and gets no termination pay. On 25 May,

they sustain personal injury and become unable to work. There is no indication they had a job to go to.

They become unable to work within 28 days of ceasing work, so the first criterion is met, but they do not have a job to

go to within 3 months of DOFI and therefore this person is not eligible for extension of employee earner status.

NOTE Example 2

A person works every year in a fruit pack house from December to March. The person suffers an injury and becomes

unable to work within 28 days of finishing the 2009 season. The employer is contacted and confirms in writing that the

person has worked for them in the last two seasons, ie 2008 and 2009 and that there is a reasonable expectation that

the person would be called upon to work in the next season, ie 2010. The employer is confirmed as a registered em

ployer for tax and levy purposes.

ACC would accept that the person meets the extension of employment criteria and would provide weekly compen-

sation to that client.

Determine extension - employee job to go to - Reference

http://thesauce/team-spaces/chips/compensation/weekly-compensation/reference/eligibility-187/determine-extension---

employee-job-to-go-to/index.htm

under the Official Information Act 1982

Released

ACC > Claims Management > Manage Client Payments > Operational Policies > Weekly Compensation > Eligibility > Extension of Employment Status

Uncontrolled Copy Only : Version 8.0 : Last Edited Tuesday, 28 January 2020 3:25 PM : Printed Tuesday, 4 August 2020 7:33 PM

Page 5 of 5

Levy Liable Earnings (LE) Policy v9.0

Summary

Objective

Levy Liable Earnings (LE) Policy v9.0

Summary

Objective

A customer's Liable Earnings (LE) are used to calculate the amount of levies that they are liable to pay. This policy explains how the

LE is calculated for different policy types and situations.

Owner

Ronel Gerber

Expert

Christopher Brake

Policy

1.0 What are Liable Earnings?

a LE are income that a person or company has declared to IR that is liable for ACC levies.

2.0 How are Liable Earnings calculated?

a The LE calculation depends on the type of policy or if the customer is a mixed earner.