ICT Shared Capabilities

Marketplace

Managed Payroll Services

Security Risk Assessment

Report

Issued by

ICT Shared Capabilities

Marketplace

Managed Payroll Services

Security Risk Assessment

Report

Issued by

under the Official Information Act 1982

Digital Public Services Branch

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

IN-CONFIDENCE

Glossary of Terms

Availability

Ensuring that authorised users have timely and reliable access to

information.

Confidentiality

Ensuring that only authorised users can access information.

Consequence

The outcome of an event. The outcome can be positive or negative.

However, in the context of information security it is usually negative.

Control

A risk treatment implemented to reduce the likelihood and/or

impact of a risk.

Gross Risk

The risk without any risk treatment applied.

Impact

See Consequence.

Information Security

Ensures that information is protected against unauthorised access

or disclosure users (confidentiality), unauthorised or improper

modification (integrity) and can be accessed when required

(availability).

Integrity

Ensuring the accuracy and completeness of information and

information processing methods.

Likelihood

See Probability.

Probability

The chance of an event occurring.

Recovery Point Objective

The earliest point time that is acceptable to recover data from. The

(RPO)

RPO effectively specifies the amount of data loss that is acceptable

to the business.

Recovery Time Objective

The amount of time allowed for the recovery of an information

(RTO)

system or service after a disaster event has occurred. The RTO

effectively specifies the amount of time that is acceptable to the

business to be without the system.

Residual Risk

The risk remaining after the risk treatment has been applied.

Risk

The effect of uncertainty on the business objectives. The effect can

be positive or negative. However, in the context of information

security it is usually negative.

Risk Appetite

The amount of risk that the organisation is willing to accept in

pursuit of its objectives.

under the Official Information Act 1982

Risk Owner

A person or entity with the accountability and authority to manage

a risk. Usually, the business owner of the information system or

service.

Stakeholder

A person or organisation that can affect, be affected by, or perceive

themselves to be affected by a risk eventuating.

Threat

A potential cause of a risk.

Released

Vulnerability

A weakness in an information system or service that can be

exploited by a threat.

Managed Payroll Services SRA

IN-CONFIDENCE

Page 4 of 51

IN-CONFIDENCE

Contents

Glossary of Terms

4

Executive Summary

6

Introduction

6

Key Risks

7

Gross Risk Position

8

Key Recommendations

9

Residual Risk Positions

11

Business Context

13

Business Processes Supported

13

Information Classification

16

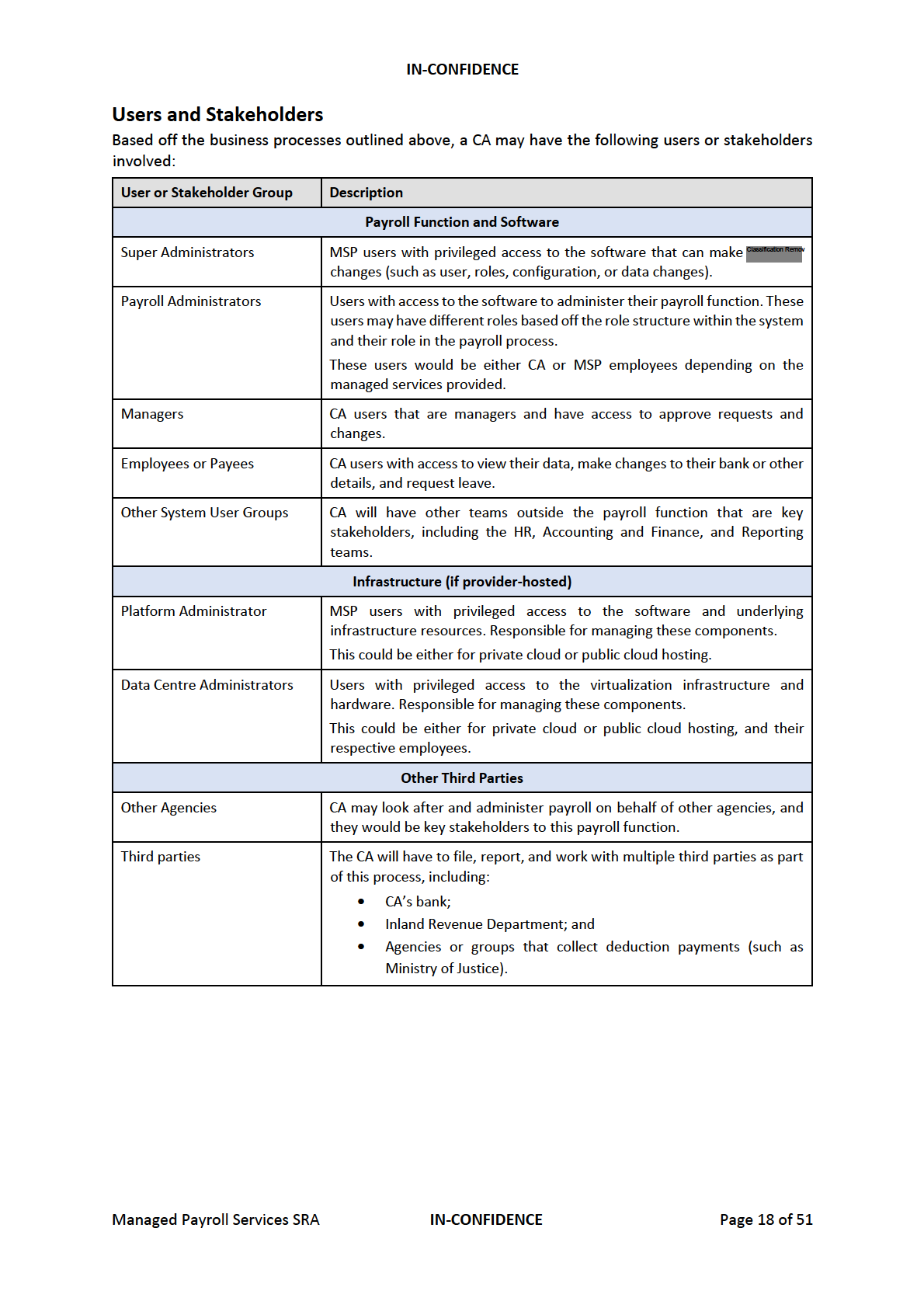

Users and Stakeholders

18

Legislation, Policy, and Guidelines

19

Technical Context

20

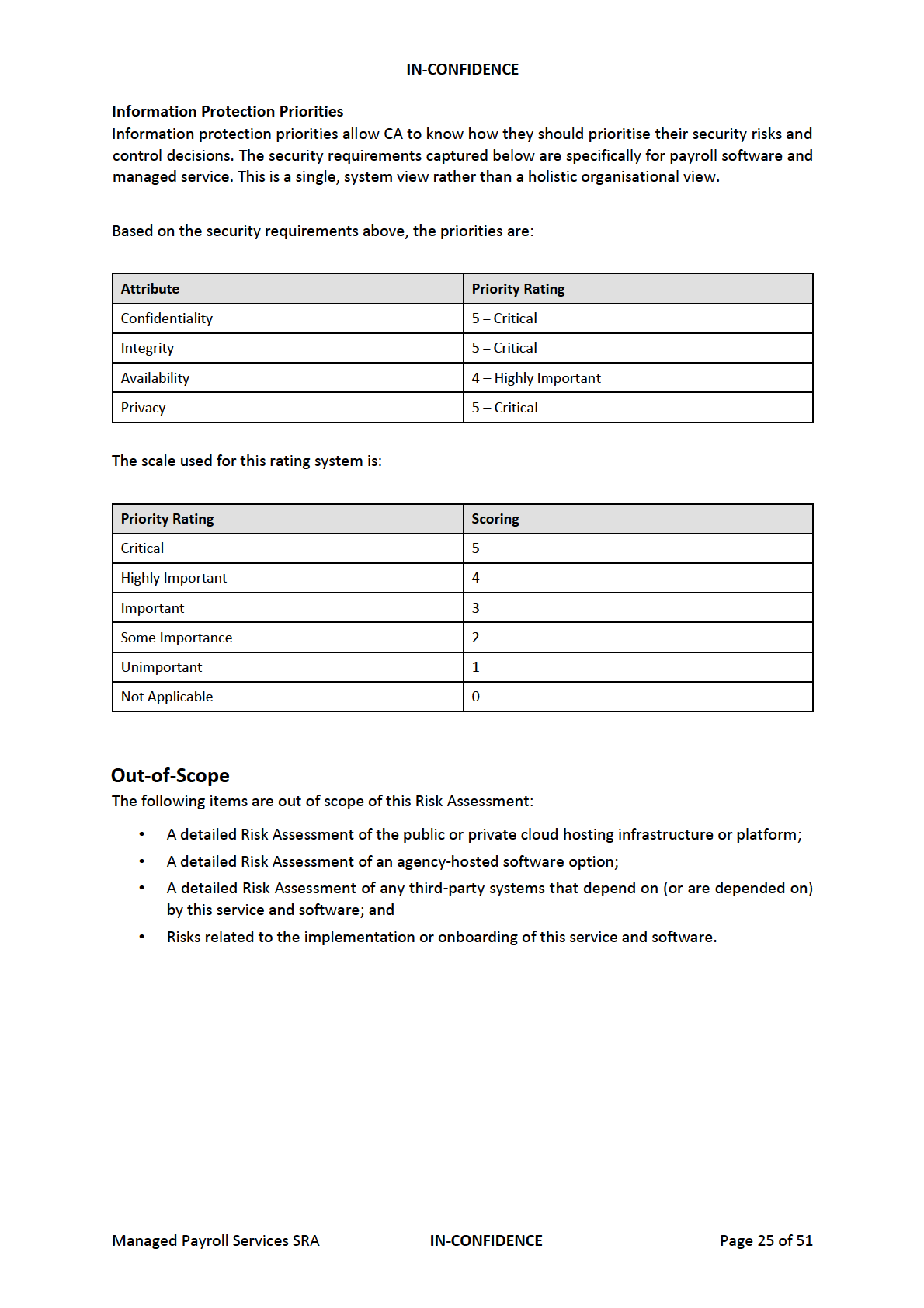

Security Requirements

23

Out-of-Scope

25

Detailed Findings

26

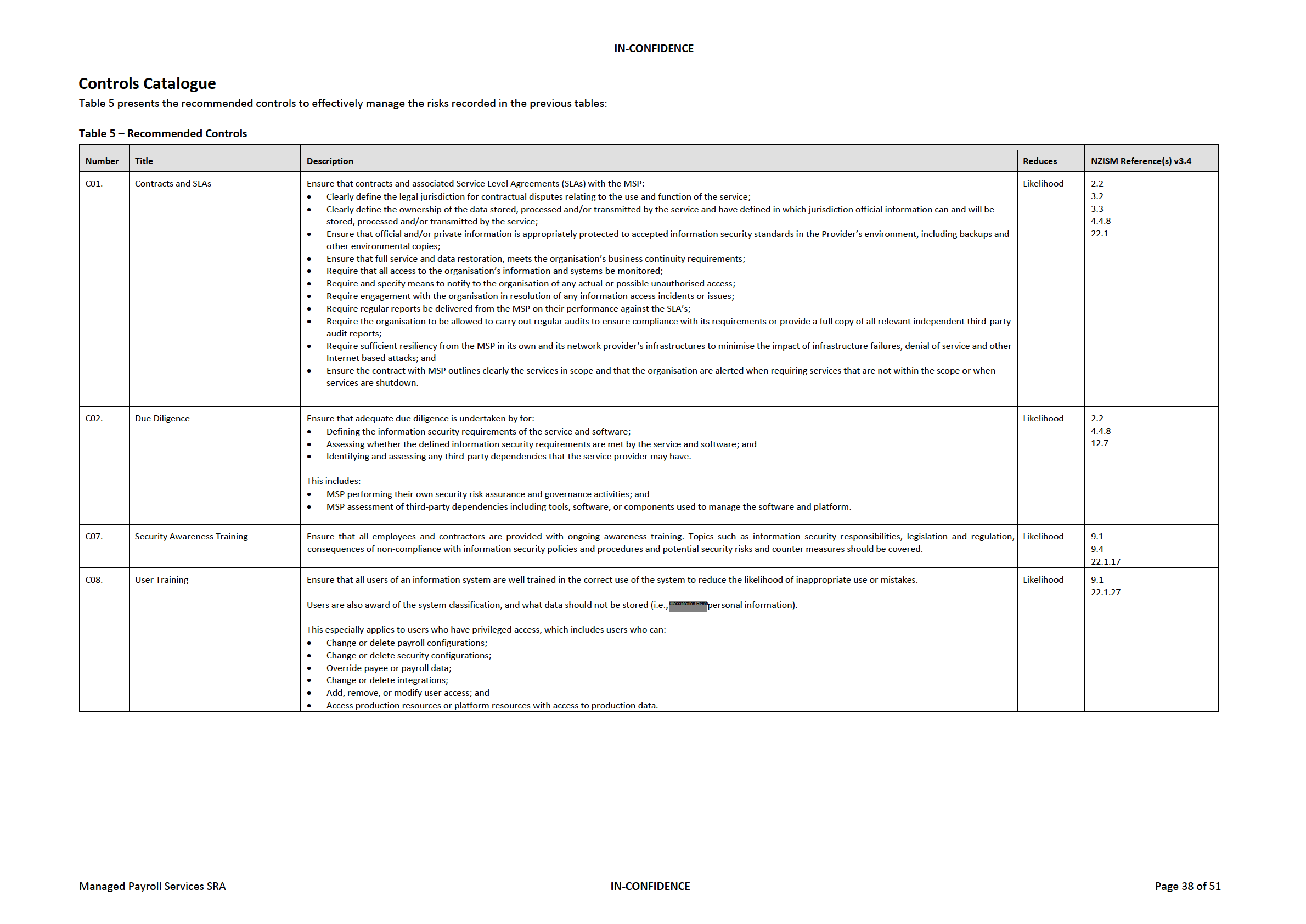

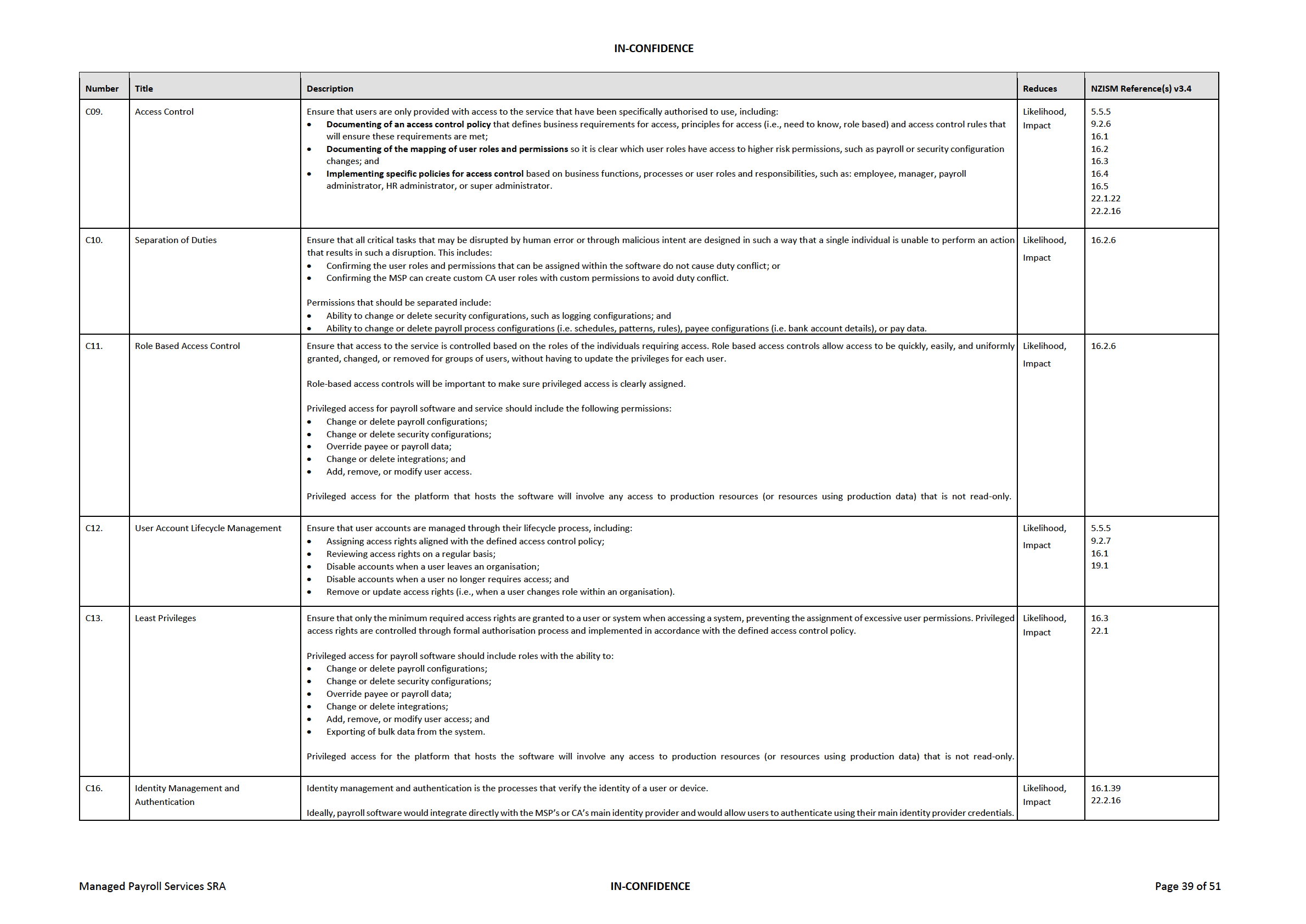

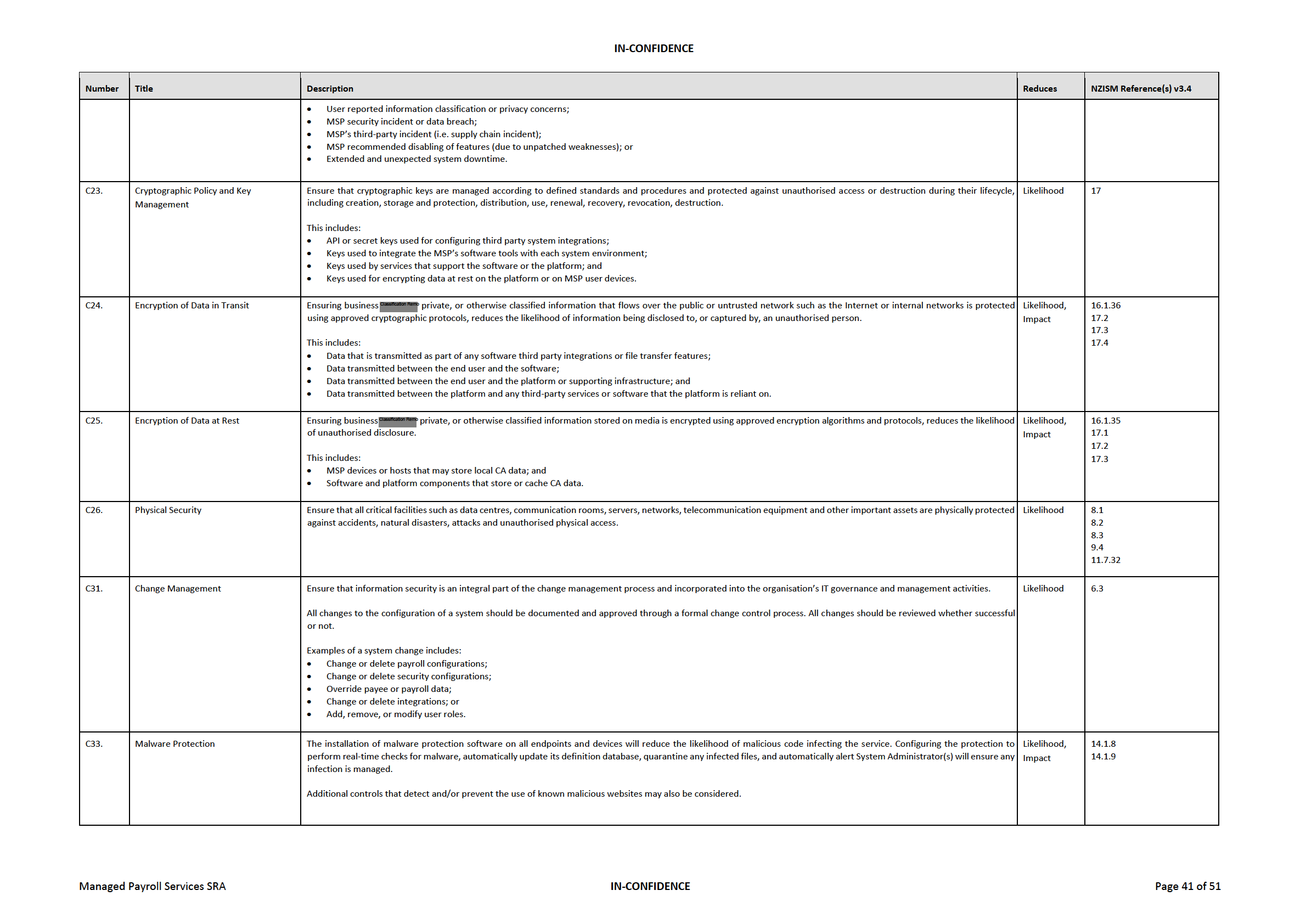

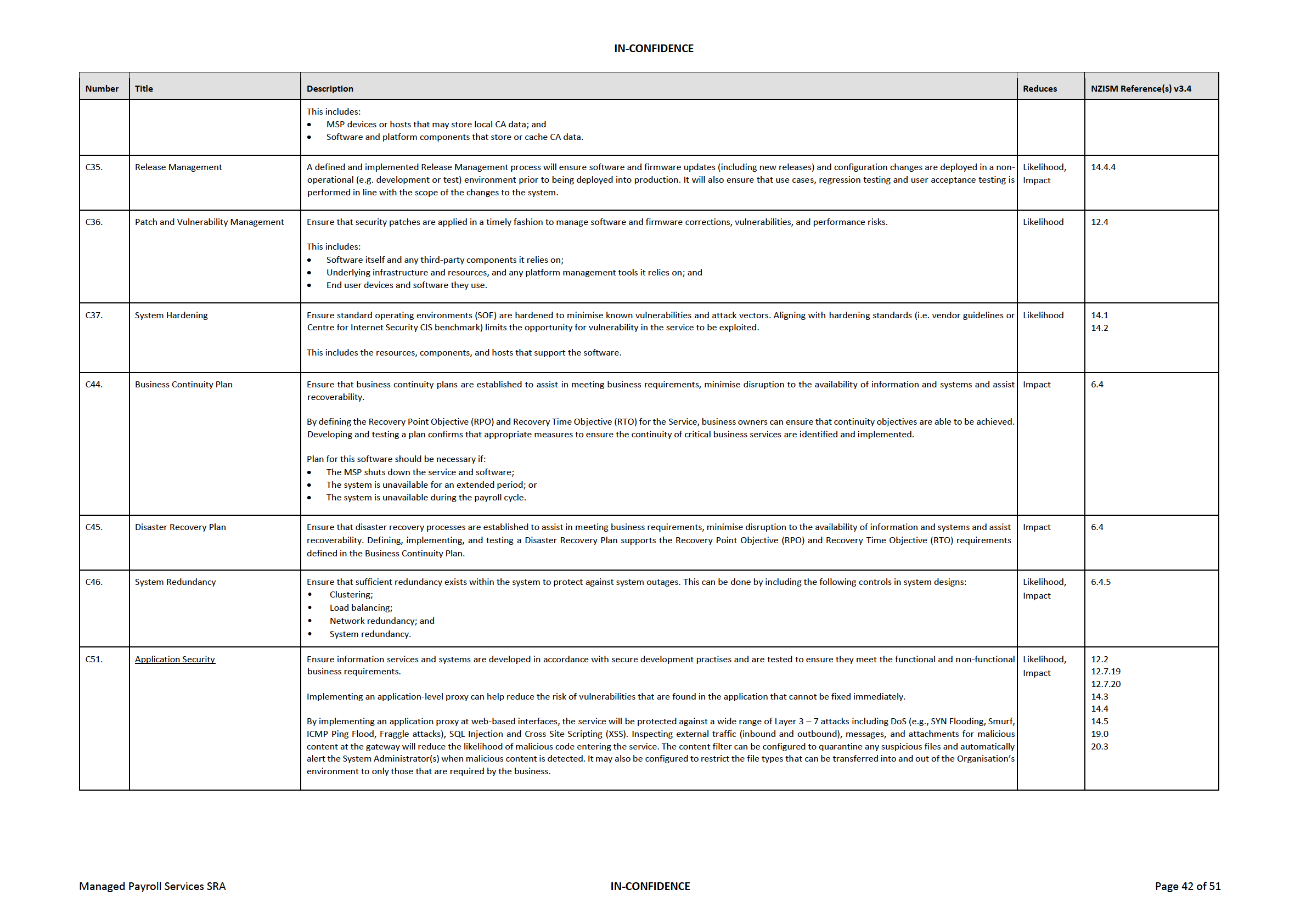

Controls Catalogue

38

Appendix A – Consulted Agencies and Suppliers

46

Appendix B - Project Overview

47

Scope

47

Approach

48

Appendix C – Risk Assessment Guidelines

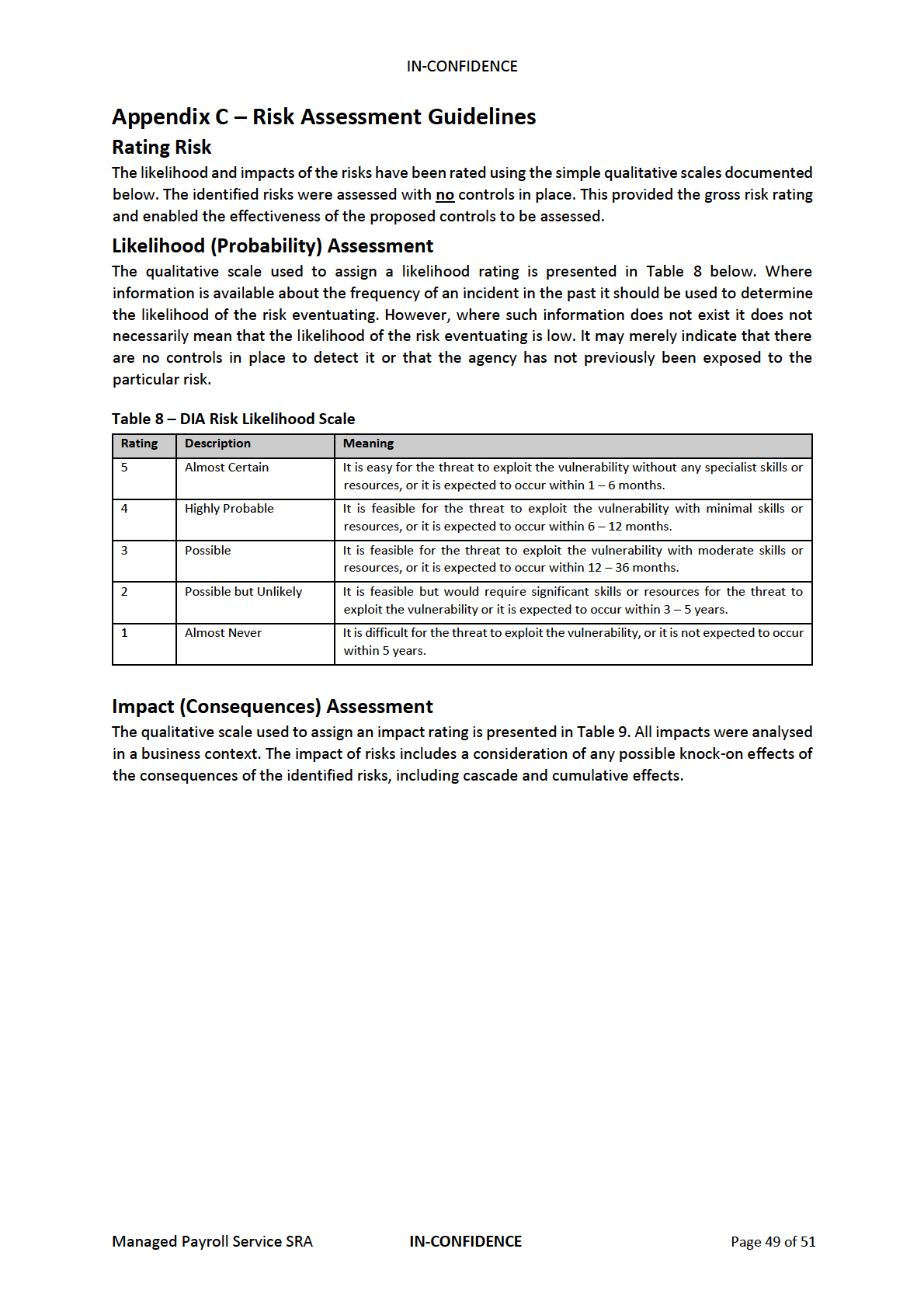

49

Rating Risk

49

Likelihood (Probability) Assessment

49

Impact (Consequences) Assessment

49

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 5 of 51

IN-CONFIDENCE

Executive Summary

Introduction

Payroll is a large, important, and complex part of an Agency. To effectively run payroll services, the

software used must integrate with many different systems. All these systems combined perform key

business functions ranging from payroll, time and attendance, award interpretation, rostering, human

resources, workforce management, self-service, and data management.

Payroll itself is made up of two channels:

• Managed Services, which includes both software and a range of associated business and

supporting services; and

• Enterprise Software, which includes the software.

The Marketplace Managed Payroll Service catalogue may rely on either provider-hosted (or Software-

as-a-Service, SaaS) or agency-hosted software.

This report includes the findings for the information security Risk Assessment for the Managed Payroll

Service, reliant on provider-hosted software and used by Consuming Agencies (CA). There will be

multiple suppliers (referred to as Managed Service Providers, MSP) that will provide this service, and

each CA will have their own unique context and risk appetite. Therefore, this report contains generic

findings, and the intent is that each CA will review them using their own risk management framework.

This Risk Assessment also only considers the context that the data stored, transmitted, or processed

by these products is classified as IN-CONFIDENCE or lower. If a CA stores, transmits, or processes data

with a higher classification, they will need to re-assess these risks using their own information

classification policy and risk management framework.

Only provider-hosted software options are considered in-scope for this assessment. This means this

assessment will include risks relating to the MSP:

• Managing and administering payroll functions and business processes on behalf of a CA;

• Managing and performing software support for provider-hosted software (i.e. management

of CA tenancy data, configurations, and users); and

• Managing or sharing responsibility for the underlying software infrastructure (i.e.

under the Official Information Act 1982

management of all other components of the software stack).

The details of the Marketplace structure and security risk assurance framework can be found in

Appendix B.

The Risk Assessment performed followed the Government Chief Information Officer’s (GCIO) Risk

Assessment process, which is based on the AS/NZS ISO 31000:2009 and ISO/IEC 27005:2011 risk

Released

management standards.

Managed Payroll Services SRA

IN-CONFIDENCE

Page 6 of 51

IN-CONFIDENCE

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 7 of 51

IN-CONFIDENCE

9(2)(k)

Gross Risk Position

Error! Reference source not found. illustrates the rating of each risk without any controls in place

.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 8 of 51

IN-CONFIDENCE

Key Recommendations

The Risk Assessment included key controls that if implemented, would help to address the identified

risks. A Controls Validation Plan (CVP) was also developed to specify the recommended controls

outlined in the Risk Assessment.

9(2)(k)

To mitigate and manage the identified gross risks rated as

9(2)(k) the following key recommendations should be undertaken:

1. MSP Due Diligence

Most of the recommended security controls must be implemented and managed by the MSP, or

the MSP must perform their own due diligence and share the management of the control with

another third party (such as a public cloud hosting provider). This includes controls for:

• Access controls and management;

• System resiliency, redundancy, and recovery;

• Encryption (in-transit and at-rest);

• Change and configuration management;

• Endpoint and host hardening and protection;

• Secure development and operations management; and

• Internal training.

While it is unlikely that the CA will be able to influence or dictate how the MSP manages these

controls, it is important to make sure the CA is aligned with the MSP before they enter into a

contract or start sharing data.

2. Access Management

The highest risks in this assessment relate to unauthorised access and misuse of access. While

most of these risks sit with the MSP, it will be critical for the CA to consider their own access

controls. Although CA users may have limited access to self-service or Manager permissions, this

can still be misused and lead to significant impacts to the CA.

This includes integrating the software with the CA’s own identity provider, or at least having

security controls configured to enforce two-factor authentication. It also means making sure that

under the Official Information Act 1982

logging is configured so the MSP or CA could be notified when events happen that need to be

investigated, such as failed login attempts or multiple bank account changes. It also includes

making sure there are granular enough permissions so high-risk requests, such as bank account

changes, can be approved by a manager or other role.

3. Incident Response and Resiliency Planning

Given the high-risk nature of a payroll function, it is important to balance out preventative controls

with detective controls. That way if a control fails, it can still be detected. This is especially the

Released

case where permissions might not be granular enough to require a second level of approval before

making a high-risk security configuration change.

Logging and alerting will depend on the software and managing this will be the responsibility of

the MSP. This does not mean the CA does not have to be concerned with this risk. The CA should

Managed Payroll Services SRA

IN-CONFIDENCE

Page 9 of 51

IN-CONFIDENCE

be prepared to respond if the MSP raises an incident with them and should have a clear plan for

how those incidents are to be treated and escalated. The same goes for resiliency planning. If the

software is unavailable and the MSP is working to recover the system, the CA should be prepared

and aware of their plan of action as they will remain responsible for paying their payees. This could

involve a business continuity plan or a severe incident response playbook, including the option to

issue last month’s pay while the issue is resolved.

4. Additional Assessments

This Risk Assessment is expected to cover most of the use cases for a CA that wishes to use a

managed payroll service and software. However, there will be a few edge cases that might apply

that can have large impacts to security risk. This includes edge cases related to:

• Initial migration from the previous payroll system;

• Overseas legislation;

• Use or storage of Classification Removed data; and

• Limitations of software hosted overseas (i.e. jurisdictional, performance, operational risks).

A CA should consider if these edge cases apply to their context and perform additional risk or

assessment work to fully understand how this context affects these risks.

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 10 of 51

IN-CONFIDENCE

Residual Risk Positions

Table 2 below illustrates the expected residual rating of each of the risks if all the recommended MSP

controls are implemented and appropriately configured and managed.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 11 of 51

IN-CONFIDENCE

Table 3 below illustrates the expected residual rating of each of the risks if all the recommended CA

controls are implemented and appropriately configured and managed.

Table 3 – CA Residual Risk Ratings

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 12 of 51

IN-CONFIDENCE

Business Context

This section provides an overview of the generic business context for the Managed Payroll Services

that are in scope of this generic information security Risk Assessment.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 13 of 51

IN-CONFIDENCE

9(2)(k)

Pre-payroll Services Processes

Recording of pay data involves many factors:

•

Salary or rostered wages;

•

Schedules or work patterns (default, or custom); and

•

Pay rules (award interpretation, or deductions and allowances)

Salary

under the Official Information Act 1982

Salaried employees have a pattern set in their work profiles that determines how pay is calculated,

and this would be configured and set in the payroll system. There is a default pattern that represents

a common, standard salaried employee (such as Monday to Friday, 8AM to 4PM).

This pattern can be changed and is often happens due to different pattern terms in the salaried

employee’s individual agreement or collective agreement, change in part-time or full-time status.

Released

Rostering / Time and Attendance

Payees paid according to a roster can be full-time, part-time, or casual employees. If a payee is on

rostered wages, the time that they are paid for is based on either rostering (hours recorded in

advance) or a time and attendance (hours recorded

already worked). Either could be performed:

Managed Payroll Services SRA

IN-CONFIDENCE

Page 14 of 51

IN-CONFIDENCE

•

Manually, such as using spreadsheets and entering data into a system; or

•

Using a system, either within a separate rostering system or within the payroll software (as an

add-on feature).

There are common controls and processes followed to confirm the integrity of the hours before the

payroll process kicks off:

•

Default schedules and configurations – These are set in the rostering or time and attendance

systems, and make sure the pay is correct and complies with the Holidays Act;

•

Approval flows - Hours recorded would go through an approval flow and the approvers

required would depend on either: delegation matrix, collective agreement, individual

agreements, or multi-employer agreements; and

•

Data integrity reports – These can be run in the payroll systems to confirm the pay calculated

is accurate, complete, and reliable.

Pay Rules

Last part of recording pay correctly involves pay rules and this involves considering any award

interpretation, allowances, and deductions that might apply to a specific payee.

Award interpretation involves the translation of worked hours into a paid value based off rules and

regulatory requirements set in the system. This can include allowances, overtime, and penalties. The

rules and requirements are configured in either:

•

The separate rostering systems; or

•

Within the payroll software (as an add-on feature).

Common deductions that need to be configured before payroll is run includes:

•

Employment or contract status;

•

Salary sacrifice (or a donation of part of their salary to a charity);

•

Kiwisaver or superannuation contributions;

•

Inland Revenue Department or Ministry of Justice fines;

•

Student loan payments;

•

Any other changes agreed (such as overpayments, payment of leave up-front); and

•

Payroll tax.

under the Official Information Act 1982

Payroll Processes

The payroll process for each CA will vary, but there are some common steps taken including:

•

Data integrity reporting and validation;

•

Trial pay runs;

•

Calculation of pay;

•

Final pay run and generation of pay, bank, and other third-party files; and

•

Repeat of process for multiple pay runs (i.e. multi-agency payroll).

Released

Pay Calculations

Pay calculation may start off with the data that is imported in from other systems 9(2)(k)

9(2)(k)

or it will start off with data based off the profile and rules that the

payee is set up with in the payroll system.

Managed Payroll Services SRA

IN-CONFIDENCE

Page 15 of 51

IN-CONFIDENCE

These calculations are consistent across agencies due to required compliance with the Holidays Act,

however they still need to be configured within the system. The CA can alternatively follow the

common process model, which helps the CA make sure the payroll rules configured meet good

practice and legislative requirements.

Pay Runs

A CA may administer multiple pay runs before pay is finalised. It may involve a trial run, which checks

if the CA is not under or overpaying. Multiple checks take place including checking number of payees

compared to number of employees, comparing of pay data to previous pay runs. These results are

also needed for audit evidence.

When the final run is administered, multiple files will be generated and may include (but is not limited

to):

•

Bank files – which are transferred to the CA’s bank for payment to payees;

•

IRD files – which are transferred to IRD for tax and other compliance;

•

Payees pay information – which includes a summary of their pay, allowances, and deductions;

•

3rd party files – for uploading of pay data into other systems the CA may use (such as financial

management or accounting systems), or to other 3rd parties that deductions were made for

(such as Ministry of Justice); and

•

Union files – which includes a summary of union fees that have been paid.

These files may be manually transferred (by manually uploading the files to the other system) or there

may be an integration or file transfer system used by the CA.

For CA that look after multiple agencies’ payroll, this process would repeat for each agency they look

after.

Post-payroll and Ongoing Processes

After the payroll run is complete, a CA will perform:

•

Accounting and recording of the pay run; and

•

Reporting and sharing of reports with groups within the CA or agencies they administer payroll

for.

There will also be ongoing services that take place outside of the payroll run, such as:

under the Official Information Act 1982

•

Software data management (such as configuration management of profiles, pay rules, and

other payroll-related configurations, access management, and data management);

•

Integration management (such as Rostering, Time and Attendance, HR, and bank system

integration);

•

Identity Provider integration (for authentication to the system);

•

Software, infrastructure, and hardware management; and

•

Supporting procedural controls (such as incident response, disaster recovery, and business

Released

continuity).

Information Classification

The security classification of the information that will be stored, processed, or transmitted by the

payroll software and the MSP has been evaluated as IN-CONFIDENCE and below. This is because while

Managed Payroll Services SRA

IN-CONFIDENCE

Page 16 of 51

IN-CONFIDENCE

the payroll software, managed service provider, and business processes use personal information, this

data would not cause an impact to diplomatic, economic wellbeing, safety, or operational

effectiveness of New Zealand.

There is a risk that the payroll software and service may store Classification Remove information. The most common

situations include:

•

Data or documents uploaded related to leave taken that involves domestic violence,

vulnerable children, or health information.

If CA wish to consume the software and service for information classified to Classification Removed

CAs will need to comply and confirm with controls detailed in the Protective Security Requirements

(PSR).

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 17 of 51

under the Official Information Act 1982

Released

IN-CONFIDENCE

Legislation, Policy, and Guidelines

CA must ensure that they can demonstrate compliance with applicable legislation, policies, guidelines,

and any other external requirements when using payroll software and services.

The following legislation, policy, and guidelines relate specifically to security requirements are

considered relevant to most CA:

• Protective Security Requirements (PSR); and

• New Zealand Information Security Manual (NZISM v3.4).

The following legislation, policy, and guidelines relate different aspects to the payroll function or the

business processes they support:

• Holidays Act 2003;

• Human Rights Act 1993;

• Privacy Act 2020;

• Income Tax Act 2007;

• Employment Protection Act 1987;

• Live Organ Donors Act 2016;

• Public Records Act 2005;

• Minimum Wage Act 1983;

• Official Information Act 1982;

• Parental Leave and Employment

• Kiwisaver Act 2006;

Protection Act 1987;

• Accident Compensation Act 2001;

• Public Finance Act 1989;

• Child Support Act 1991;

• Student Loan Scheme Act 2011;

• Datacom GSF Specifications;

• Support Workers (Pay Equity)

• Domestic Violence Amendment;

Settlements Act 2017;

• Employment Relations Act 2000;

• Tax Administration (Correction of

• Equal Pay Act 1972;

Errors

in

Employment

Income

• General Disposals Authority 6;

Information) Regulations 2019;

• Health and Safety at Work;

• Tax Administration Act 1994;

• Home and Community Support

• Volunteers Employment Protection

(Payment for Travel Between Clients)

Act 1973; and

Settlement Act 2016;

• Wages Protection Act 1983.

Some CA may be responsible for payroll services to payees who must comply with overseas legislation.

There will be different requirements and impacts if these are not followed and were not considered

in the context of this work. The CA should perform their own assessment when understanding their

specific requirements under any legislation.

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 19 of 51

IN-CONFIDENCE

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 20 of 51

IN-CONFIDENCE

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 21 of 51

IN-CONFIDENCE

9(2)(k)

Service Owner and Experts

Each CA will use this Risk Assessment and apply it to the specific MSP and payroll software solution

they selected from the Marketplace, and to their own internal risk framework and context. As part of

that, the CA can get support from the following stakeholders:

•

Senior Responsible Officer – or the officer responsible for the use and risk of the software in

their agency;

•

IT Security Manager – or the manager responsible for performing security assurance for the

system;

•

Solution Architect – or the architect responsible for identifying the technical components and

features in the MSP and software chosen; and

•

Payroll and other subject matter experts – or others in the CA who can assist with adjusting

this Risk Assessment in the context of how the system will be used within the CA.

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 22 of 51

IN-CONFIDENCE

Security Requirements

The security requirements help inform the technical impact of the security risks captured, and the

requirements vary based off the confidentiality, integrity, availability, and privacy requirements of the

data used by the payroll system.

The exact security requirements will vary by CA and will require the CA to assess using their

framework. In most cases, the impacts across a CA will be similar. Those impacts have been defined

below.

Confidentiality and Privacy

The payroll system and service will store, process, and transmit information that includes Personally

Identifiable Information (PII), and limited Classfication

Removed information that may be included in their leave,

allowance, and deduction requests. This information is considered IN-CONFIDENCE.

There are different ways this information’s confidentiality or privacy could be compromised: an

administrative or system user could accidently or intentionally share data exports, pay files, or reports;

the system could be mis-configured which would allow other system users to see data they shouldn’t

be allowed to see; a CA’s account could be inappropriately accessed leading to a data breach; the MSP

could have a security incident relating to their staff or the system which leads to a data breach.

The impact of a confidentiality or privacy incident would vary, and it would depend on the amount of

information involved. If there was a small amount of information involved, the impact to the CA would

be

moderate. If there was a large of amount of information, the impact would be

significant. It could

result in:

•

Breach of laws, resulting in litigation and against the CA (and other agencies they provide

payroll services for);

•

Significant reputational and political damage;

•

Loss of confidence in the security of the software;

•

Significant ongoing operational and service delivery impact to the CA due to incident

investigation and process changes;

•

Significant financial impact due to the need for additional resources to assist with the

investigation and resolve any issues, and for any litigation fees; and

•

Minister and leadership briefing and updates.

under the Official Information Act 1982

Integrity

The payroll system is a key component of the overall payroll function within a CA. They rely on the

accuracy and integrity of the data in the system for payroll processes as well as supporting business

processing (such as financial reporting and HR).

There are different ways the information’s integrity could be compromised, and most of those events

come down to access controls (including user access and data separation). The impact would also vary

Released

and would depend on the amount of information that was modified. If there was a small amount of

information involved, the impact to the CA would be

moderate. If there was a large of amount of

information, the impact would be

significant. It could result in:

•

Breach of laws (such as Holidays Act due to incorrectly calculated pay);

•

Significant reputational and political damage;

Managed Payroll Services SRA

IN-CONFIDENCE

Page 23 of 51

IN-CONFIDENCE

•

Loss of confidence in the security of the software;

•

Significant ongoing operational and service delivery impact to the CA due to incident

investigation and process changes;

•

Moderate financial impact due to the need for additional resources to assist with the

investigation and resolve any issues, and for any litigation fees; and

•

Minister and leadership briefing and updates.

Availability

Payroll is a regularly occurring process and is heavily relied on by multiple stakeholders (as captured

above under Users and Stakeholders).

There are different ways the availability of the system, service, or information could be compromised.

It could be unavailable for a short period of time due to a breaking change or misconfiguration, or it

could be unavailable for an extended period due to a prolonged Distributed Denial of Service (DDoS),

Denial of Service (DoS), or security incident with the payroll software and Provider.

If the system were unavailable outside of the pay run part of the process (less busy period), the impact

would be

moderate. If the system were unavailable during the pay run part of the process, the impact

would be

significant. It could result in:

•

The CA standing up an incident response or business continuity team to administer the pay

run without the payroll software;

•

Increased operational and service delivery impacts due to manual processing and post-

incident system updates;

•

Significant reputational and political damage;

•

Financial impact due to additional resources needed to administer manual pay runs; and

•

Leadership and Minister briefing and updates.

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 24 of 51

under the Official Information Act 1982

Released

IN-CONFIDENCE

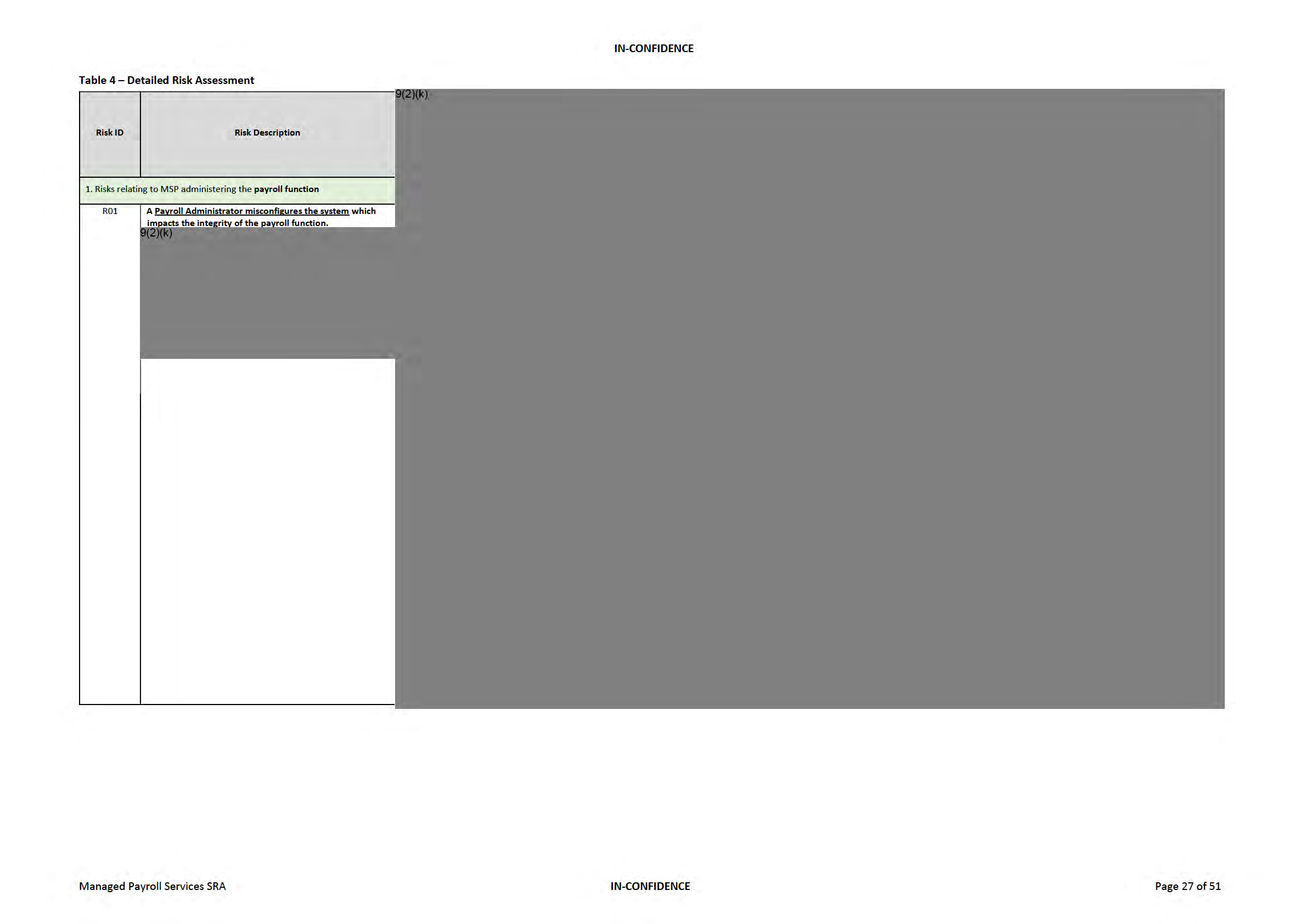

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 26 of 51

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

IN-CONFIDENCE

9(2)(k)

9(2)(k)

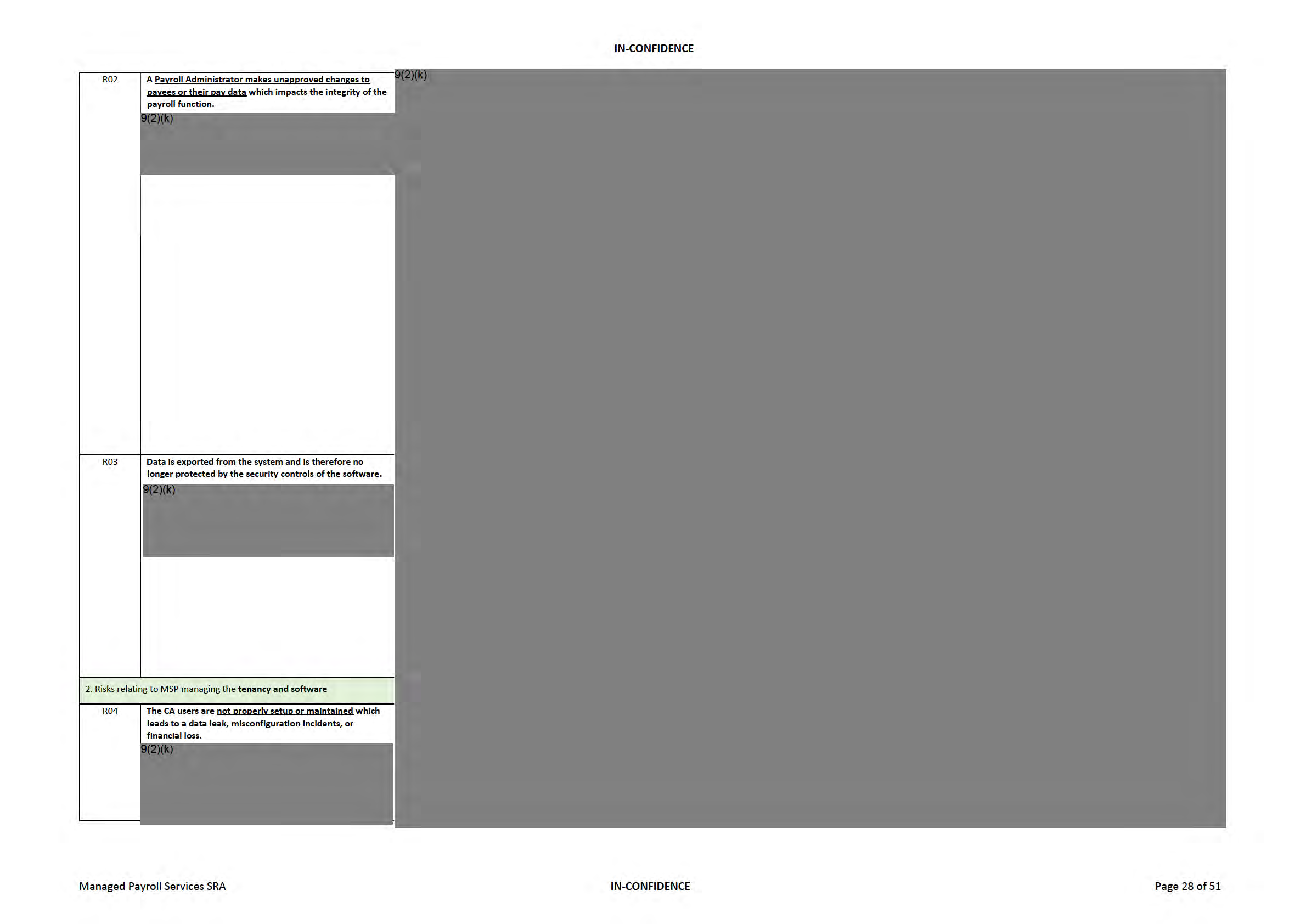

R05

A Super User misconfigures the system which impacts the

security of the system.

9(2)(k)

R06

A CA user account is inappropriately accessed which leads

to a data breach or fraud.

under the Official Information Act 1982

9(2)(k)

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 29 of 51

IN-CONFIDENCE

R07

An MSP user is inappropriately accessed which leads to a

9(2)(k)

data breach or misconfiguration incidents.

9(2)(k)

R08

An integration with another CA system is not secured

which leads to a data leak.

9(2)(k)

R09

An integration with a third-party system is not secured

which leads to a data leak.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 30 of 51

IN-CONFIDENCE

9(2)(k)

R10

Data sent to the payroll software via another system

integrations is compromised which leads to an integrity

incident.

9(2)(k)

R11

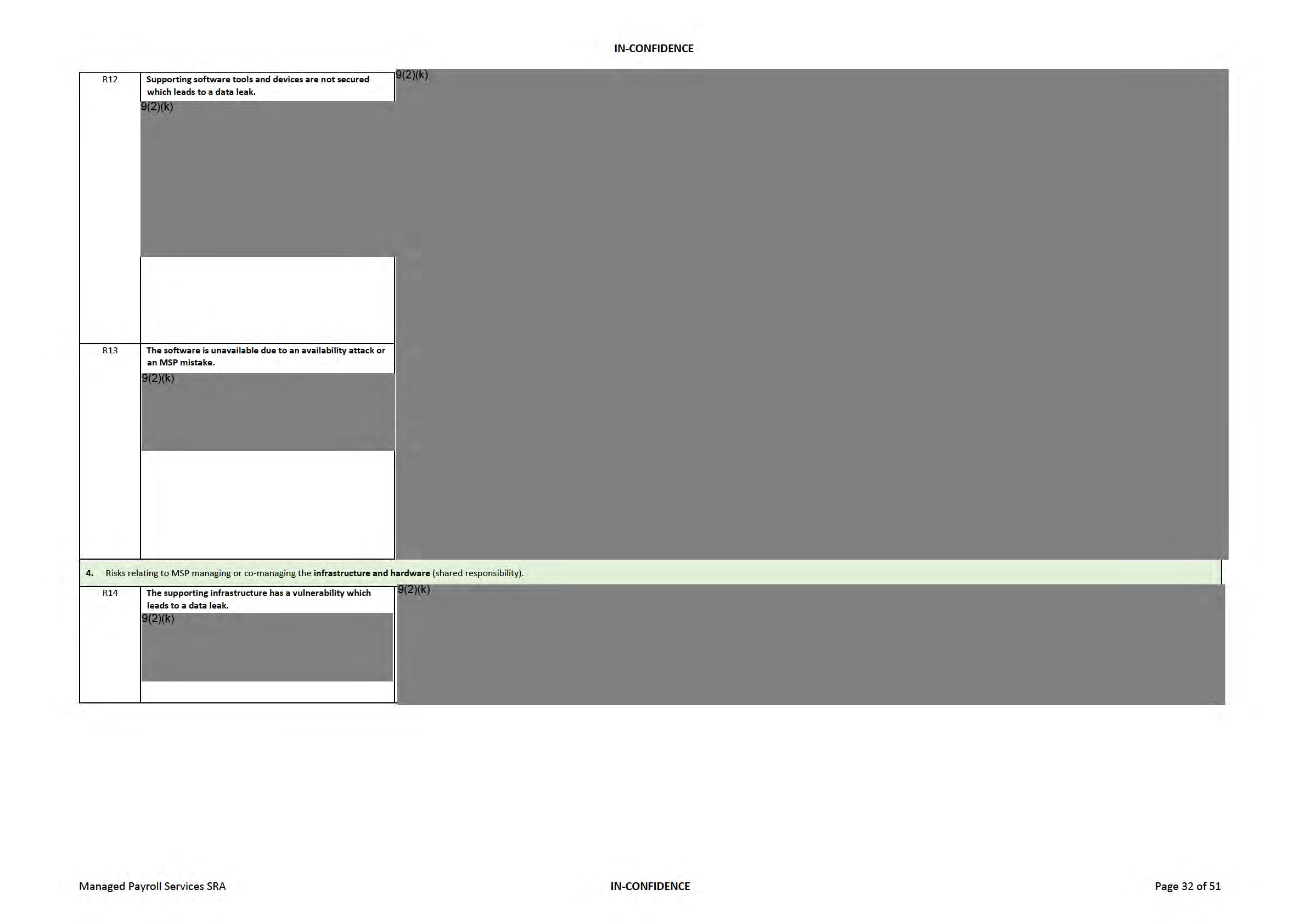

The software has a vulnerability which leads to a data

leak.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 31 of 51

under the Official Information Act 1982

Released

IN-CONFIDENCE

9(2)(k)

R15

The supporting infrastructure is not hardened or is

misconfigured which leads to a data leak.

9(2)(k)

R16

The platform is unavailable due to an availability attack,

malware infection, or an MSP mistake.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 33 of 51

IN-CONFIDENCE

9(2)(k)

R17

A Platform Administrator user account is inappropriately

accessed which leads to a data breach or misconfiguration

incidents.

9(2)(k)

R26

The MSP has a physical security breach which leads to data

loss or availability issues.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 34 of 51

under the Official Information Act 1982

Released

IN-CONFIDENCE

9(2)(k)

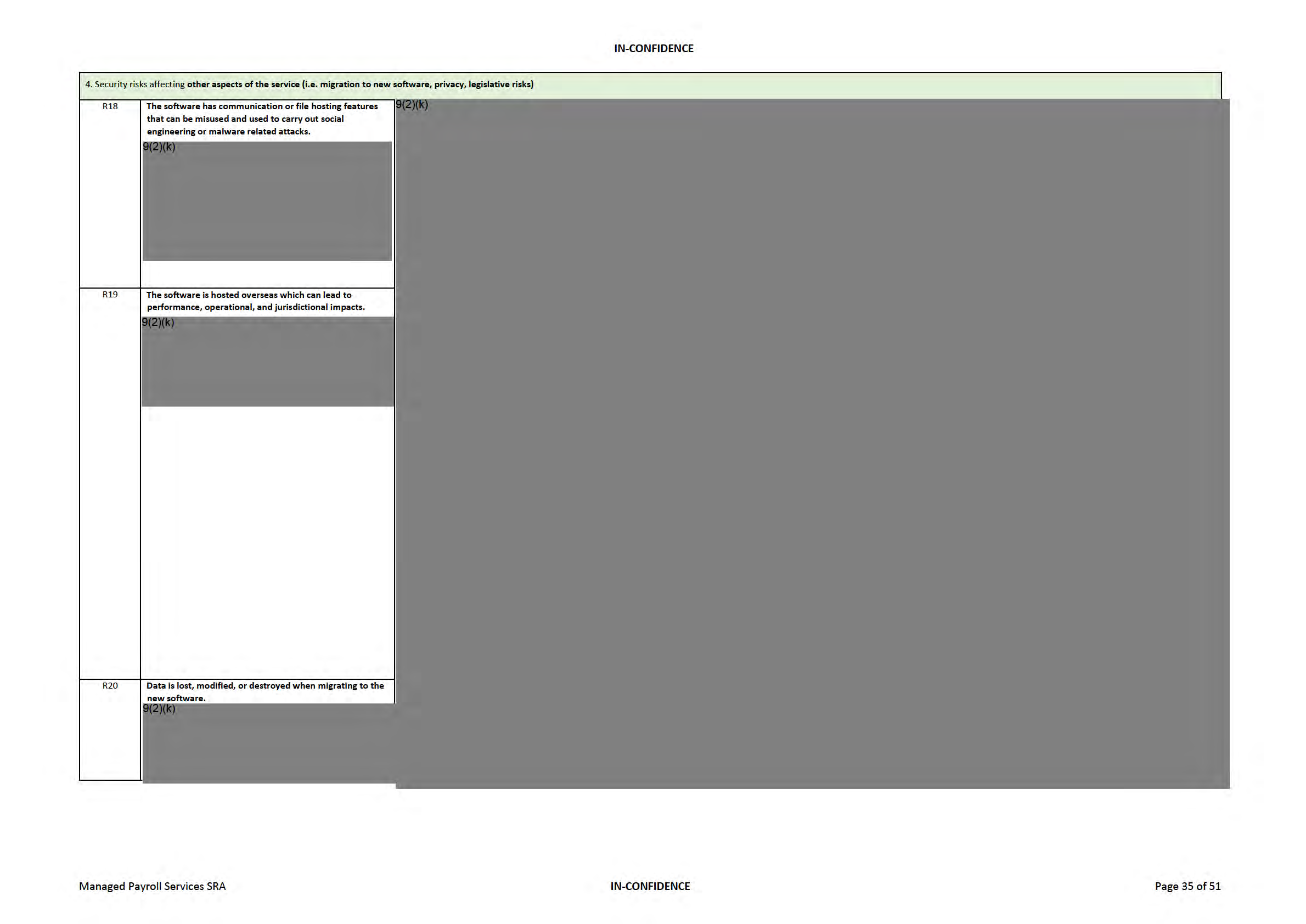

R21

Class fication

Remo

data is entered into the software which can

cause the technical and business impact of any other risk

event to be higher.

9(2)(k)

R22

A CA fails to comply with overseas legislation due to a

misconfiguration, data leak, or other security event.

9(2)(k)

under the Official Information Act 1982

R23

A CA has a different operating model which means this

assessment might not accurately capture their risks and

recommended controls.

9(2)(k)

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 36 of 51

IN-CONFIDENCE

9(2)(k)

R24

A remote working user does not secure their device which

leads to a data leak.

9(2)(k)

R25

A system that the MSP relies on has a breach which affects

the CA and their data.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Services SRA

IN-CONFIDENCE

Page 37 of 51

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

IN-CONFIDENCE

Table 6 shows which controls (that are recommended for both the MSP and CA) are related to each

risk from Table 4.

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Service SRA

IN-CONFIDENCE

Page 44 of 51

IN-CONFIDENCE

9(2)(k)

under the Official Information Act 1982

Released

Managed Payroll Service SRA

IN-CONFIDENCE

Page 45 of 51

under the Official Information Act 1982

Released

IN-CONFIDENCE

Appendix B - Project Overview

Scope

Marketplace is an AoG initiative that enables New Zealand and international businesses to offer their

products and services directly to New Zealand government agencies. Marketplace links business with

government, making the procurement process easier for all. For more details, please visit

https://marketplace.govt.nz

The Department of Internal Affairs (DIA), as Government Chief Digital Officer (GCDO), have performed

and completed this Risk Assessment report and Controls Validation Plan (CVP) to support the CA who

plan to use this Marketplace-listed catalogue service.

The objective was to create a generic Risk Assessment and CVP that would cover most of the security

risks and controls that would apply regardless of Supplier, technology, or specific context. The intent

is that this would set a baseline for the CA to use and then apply their own internal risk management

frameworks and accredit the service for their own use.

Marketplace has a list of catalogue items and suppliers that are categorised in Tier 1, Tier 2, and Tier

3. The Tier 3 a is lower entry bar for small products and suppliers where, Tier 1 is for enterprise grade

products that require the highest assurance.

For the purposes of this work, it was assumed the Managed Payroll Service would have a minimum

Tier 2 rating.

The minimum Tier rating is based on:

• Risk profile of the service;

• Use / delivery of cloud-based tools to deliver Managed Services;

• Reliance on Agency controls, particularly for people and process controls; and

• Claims made by the Supplier in the service description.

Tier 3: Baseline Index — Suppliers respond to security questions which can include the Cloud Risk

Assessment Tool (GCIO105). Assessment is based on self-assertions and not independent reviews.

SaaS go through a Confidence and Risk Index (CRI) rating by McAfee MVision.

under the Official Information Act 1982

Tier 2: Design and Control Analysis — Suppliers must provide independent security assurance

information that Consuming Agencies will be able to review. This can include ISO27001 or SOC2 Type

2 audit reports, and penetration testing reports. This information will be reviewed and confirmed

appropriate by the GCDO before Tier-2 endorsement.

Tier 1: Design and Control Effectiveness— To obtain this rating, suppliers must provide additional

information and receive Certification from the GCDO. Certification is based on Risk Assessment and

Released

demonstration of controls effectiveness can be supported from an organisation having ISO 27001 or

SOC2 Certification or going through an audit by an auditor from the SRS panel.

Managed Payroll Service SRA

IN-CONFIDENCE

Page 47 of 51

IN-CONFIDENCE

A typical Managed Payroll Service solution consists of:

• A Managed Payroll Service software package;

• A hosting service, either provided by

:

o a Public Cloud IaaS Service Provider;

o a Private Cloud IaaS Service Provider; or

o any hybrid-cloud or Government dedicated cloud IaaS Service Provider.

• The implementation of the Managed Payroll Service on the hosting service by the Supplier;

• The integration of the Managed Payroll Service with existing agency systems by the Supplier;

and

• The management and administration of the solution by the Supplier.

Approach The Risk Assessment followed the GCIO risk framework based on the AS/NZS ISO 31000:2018 risk

management standards. The assessment was conducted as a series of workshops and document

reviews, including:

• Consumption of documentation provided by DIA;

• Identification of risks and controls associated with the use of Managed Payroll Services

through a business and technical context workshop;

• Development of a Risk Assessment report in draft;

• Review of risks and ratings through a risk validation workshop; and

• Issuance of a final Risk Assessment report.

under the Official Information Act 1982

Released

Managed Payroll Service SRA

IN-CONFIDENCE

Page 48 of 51

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released

under the Official Information Act 1982

Released